⛽️📈 Will it Affect You? OPEC Cuts Oil

Happy Hump Day everyone,

In each newsletter, we try to bring to light how major news developments from around the world will impact the way you live now and into the future. Last week, we wrote an interesting piece on how a strong USD affects not only Americans but billions around the world. If you missed it, check it out here.

This week, we talk about the new OPEC+ oil cuts coming into effect in November and how our first impressions of panic may have been an overreaction once we start to peel back the curtain and take into account the facts.

Enjoy this week’s Hump Days!

- Humphrey, Rickie & Tim

Featured Story

One week prior to today, OPEC+: a group of 23 oil-producing countries including Saudi Arabia and Iraq, met in Vienna and collectively agreed to cut their output target by 2M barrels a day starting November. OPEC+ and their allies, including Russia, said the decision was based on the “uncertainty that surrounds the global economy and oil market outlooks”.

The price of Brent crude, the international benchmark started 2022 at $79 a barrel and quickly soared above $127 in March after the Russian invasion of Ukraine - the highest level in 14 years. Although, prices have been falling steadily over the past few months due to fears of a global recession, opening last week at $86. Currently, the price sits around $92.

Global daily oil consumption sits around 88M barrels/day so a 2M barrels/day cut is definitely a significant pullback. Many fear that the big cut will push inflation higher and force central banks to hike interest rates so much that it triggers a recession. This cut puts Europe in a difficult position as many European nations have imposed a price cap on Russian oil and Putin plans to withhold exports to countries that enforce that cap.

So, are we ringing the alarm bells? Not so fast. A look behind the curtain reveals many holes and so let’s brief you on what we learned.

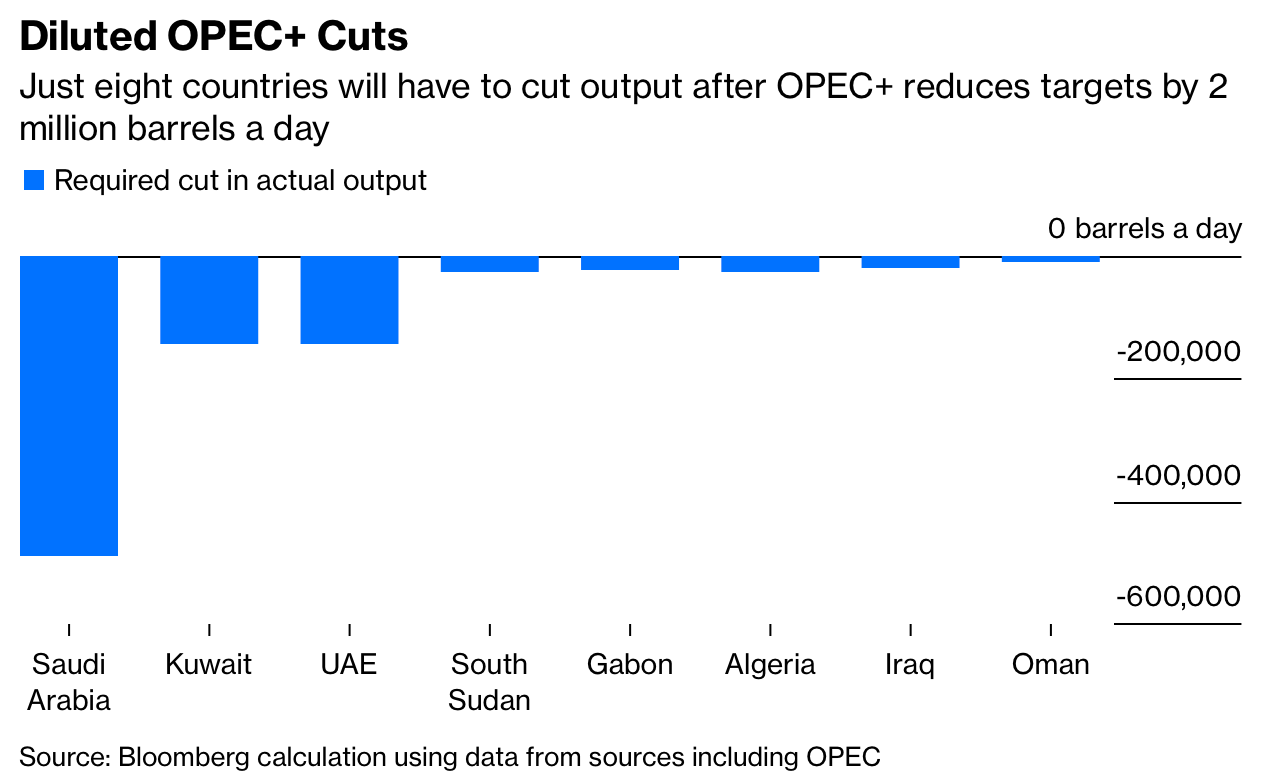

On November 1, when the target cuts come into effect, only 8/23 countries will be required to pump less crude. From the chart below, you can see that much of the burden will fall on just 3 countries: Saudi Arabia, Kuwait, and the UAE. Note that just because they agreed to a cut on paper, that does not mean that they will actually go through with it in practice. South Sudan and Gabon, for example, have had one month since the last deal came into effect (May 2020) where they were below their caps. South Sudan, in fact, not only exceeded its quota every month but was shown to have never cut a single barrel of production.

The combined cuts required of Saudi Arabia, Kuwait, and the UAE amount to 790,000 barrels/day. Should the 3 countries actually go through with these cuts, and the belief is that they will, it will be significant but quite far compared to the targeted 2M barrel/day cut. Moreover, there is a major offsetting factor at play here in Kazakhstan which is currently running more than 560,000 barrels/day below target due to maintenance at one of its biggest fields and a gas leak at another. The completion of the maintenance over the weekend should open to door for the return of another 260,000 barrels/day, and the country’s energy minister expects the gas leak to be taken care of before the end of the month - just in time to offset the planned cut.

While the planned output cut made major headlines at 2M barrels/day, with offsetting factors taken into account, the cut could be reduced to as little as 230,000 barrels/day. The global energy economy can change with a snap of a finger so next month, it could look very different - especially if Russia decides to halt production instead of accepting a capped price. For now, though, we’ve seen OPEC+ talk the talk, let’s see if they can walk the walk.

Weekly News Roundup

U.S Banks Likely Set Aside $5B in Q3 Reserves as Recession Risks Grow (Reuters)

The six biggest U.S. banks are expected to have set aside nearly $5B to cover future loan losses. With growing fears of a recession and the Fed continuing to hike interest rates to tamp down inflation aggressively, bank reserves are expected to be at the highest levels since mid-2020 and may be a huge drag on bank profits. The surge in reserves does not suggest everything is downhill, however, as Wells Fargo claims that the banking industry is more resilient with far less risk than it had before prior recessions

Oil Production Cut Could Be 10% Real, 90% Illusion (Bloomberg)

OPEC+ agreed to cut their collective output target by 2M barrels a day from November last week. The group comprises 23 countries but the burden of the cut will be shared by just three: Saudi Arabia, the United Arab Emirates, and Kuwait. It is important to note that some OPEC countries such as South Sudan and Gabon have refused to abide by the set quotas. Iraq’s national oil minister even went to assure oil buyers that the agreement would not affect his country’s exports.

Bank of England Says Pension Funds were Hours from Disaster Before it Intervened (CNBC)

The Bank of England told lawmakers that a number of pension funds were hours from collapse when it decided to intervene in the U.K. long-dated bond market last week. After a massive sell-off in government bonds - commonly known as ‘gilts’ - the central bank introduced emergency measures including a two-week purchase program and a delay on the bank’s planned gilt sales. Long-dated gilt holdings account for two-thirds of Britain’s $1.69T liability-driven investment funds (LDIs) which are largely held by salary pension plans. The unprecedented sell-off meant many funds would have likely fallen into negative net asset values and would have had to begin the process of winding up the following morning.

Charts of the Week

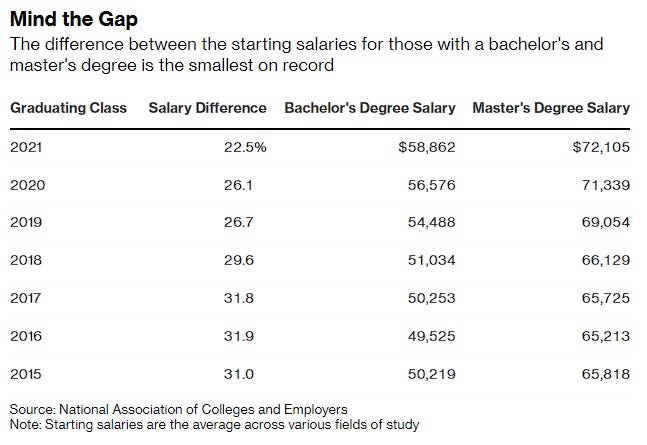

The gap between the starting salaries for those with a bachelor’s degree and a master’s degree shrunk for the fifth year in a row, adding to a debate about whether graduate school is worth the cost.