🥾🌲VF Corporation (VFC): Deep-Dive Analysis

Corporation Overview

VF Corporation owns a diverse portfolio of iconic outdoor and activity-based lifestyle and workwear brands. VF was founded as Reading Global & Mitten Manufacturing Co. in 1899 and went public on the NYSE in 1951.

VF’s portfolio of brands is based on acquiring and developing brands rather than creating, aiming to realize cost savings by finding synergies in combined operations. VF has historically been quite active with brand management, selling, and divesting brands with low future potential. It primarily sells products through its own stores, e-commerce, and at retailers such as Nordstrom.

Investment Rationale

As the chart above shows, VF Corporation has massively underperformed the broader market and the retail sector. What happened? Well for VF, it all started in 2017 with the introduction of CEO Steve Rendle.

Before Steve Rendle, VF was a disciplined company that kept leverage low and only acquired companies at attractive valuations. Its biggest two brands (Vans and North Face) were acquired when the brands were near bankruptcy. Steve had different ambitions than what VF historically was. He was attracted by the high-growth, trendy brands and wanted to bring that to VF.

The first acquisition Steve made was Williamson-Dickie, which is most known for the Dickies brand. The idea behind the acquisition was to enhance VF’s workwear segment. As seen in the table above, VF emphasized the fact that this acquisition wouldn’t impact their leverage or liquidity, noting their capacity for additional acquisitions.

VF did just that.

In 2020, VF acquired Supreme, a trendy clothing and skateboarding lifestyle brand for $2.1 billion. There were several issues with this acquisition.

Supreme was already well off its peak popularity in 2017. As seen in the Google Search trends chart above, Supreme was already on the decline as a brand.

Most of the capital used for this acquisition was debt. VF increased its net leverage ratio by over 20% for a declining brand.

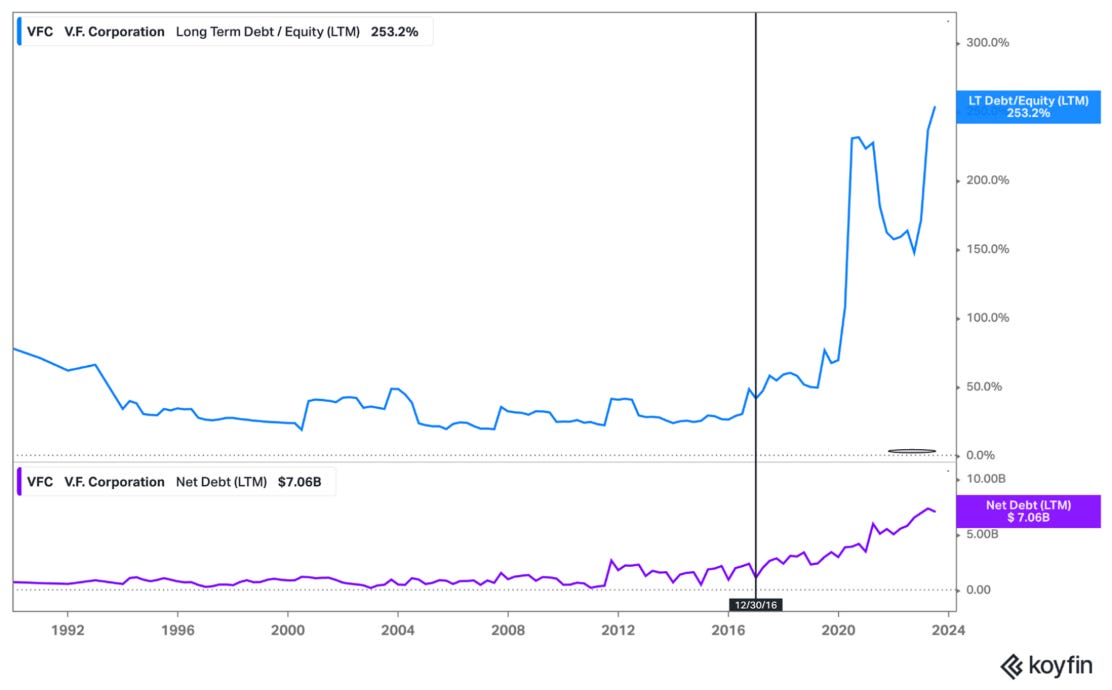

After these two acquisitions, VF found itself in deep water. It was over-levered and had more debt than at any point in the company’s history. The vertical line in the chart above shows the point in time when Steve Rendle came in as CEO, and the rest speaks for itself… Even though the amount of debt VF has is terrible and a big concern, there are actually some positives.

Most of the debt raised by VF was during a time when rates were near 0%. So their weighted average interest rate on outstanding debt is only 3.1%. Only 13% of their total debt is floating-rate.

Floating-rate debt, also known as variable or adjustable-rate debt, refers to loans for which the interest rates adjust periodically based on a predetermined benchmark or reference rate, such as LIBOR or a central bank's policy rate. The adjustments to the interest rate can occur at specified intervals, such as monthly or annually, and are designed to reflect current market conditions. As a result, the interest payments for borrowers can rise or fall over the duration of the debt, offering potential benefits of lower initial rates but carrying the risk of higher future rates.

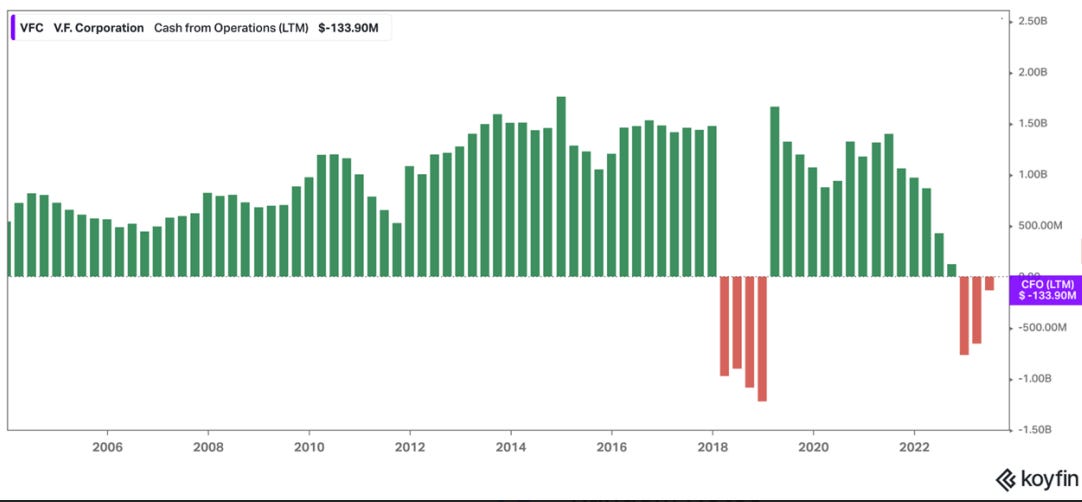

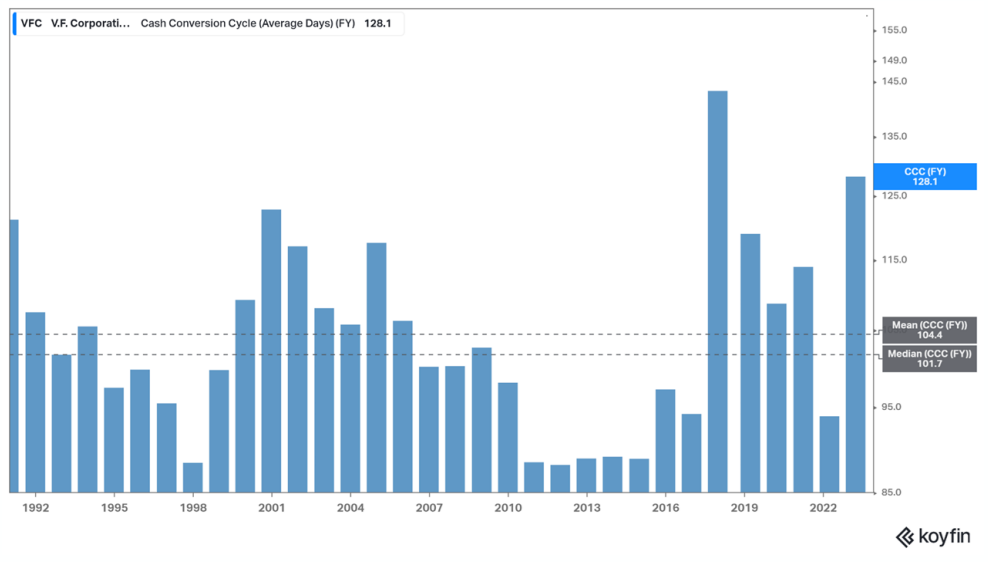

Debt and leverage wasn’t VF’s only problem. Due to supply chain issues and a pull-forward in demand due to stimulus checks, VF ordered massive amounts of inventory in 2020. By the time most of the inventory arrived, supply chains were unclogged and the pull-forward in demand started to dwindle. This led to VF holding a ton of inventory on its balance sheet. The chart below shows how long VF now has to hold its inventory before selling.

The Turnaround Plan

Eventually, enough was enough and Steve Rendle was booted from VF Corp.

VF Corp brought in Bracker Darrell, who was previously the CEO of Logitech for 11 years. During his time at Logitech, he introduced new products to help gain market share and made bolt-on acquisitions in the areas of gaming, e-sports, and streaming. He was also responsible for the turnaround of the ‘Old Spice’ brand during his time at Proctor & Gamble.

So what are some ways that Darrell can turn this company around? Well, the fixes are relatively simple.

De-Lever The Company (Debt Paydown Should Be #1 Priority)

Cut dividends or pause buybacks

VF is still paying a 50%+ dividend payout ratio, a massive source of cash that could be redirected to debt paydown.

VF spend $2.6 billion on dividends & buybacks from FY ‘21-’23.

VF has $900 million in buildings (opportunity for sale-leasebacks to raise capital)

A sale-leaseback enables a company to sell an asset to raise capital, and then lets the company lease that asset back from the purchaser. In this way, a company can get both the cash and the assets it needs to operate its business.

Spin-off smaller brands

VF has a history of selling smaller brands to private equity firms or spinning of brands as its own publicly traded entity.

Revitalize and continue to generate cash flow through existing quality brands (Vans, North Face, Dickies)

VF has brought back many old execs from the ‘glory years’ to run these brands.

Continue utilizing its Supply Chain Financing Program to lengthen DPO and decrease net CCC.

Days payable outstanding (DPO) is a financial ratio that indicates the average time (in days) that a company takes to pay its bills. A company with a higher value of DPO takes longer to pay its bills, which means that it can retain available funds for a longer duration, allowing the company an opportunity to use those funds in a better way to maximize the benefits.

The cash conversion cycle (CCC) is a metric that expresses the time (measured in days) that it takes for a company to convert its investments in inventory and other resources into cash flows from sales.

VF has utilized financing programs which led to a $100 million increase in cash from operations in FY ‘23.

Why Consider VFC Now?

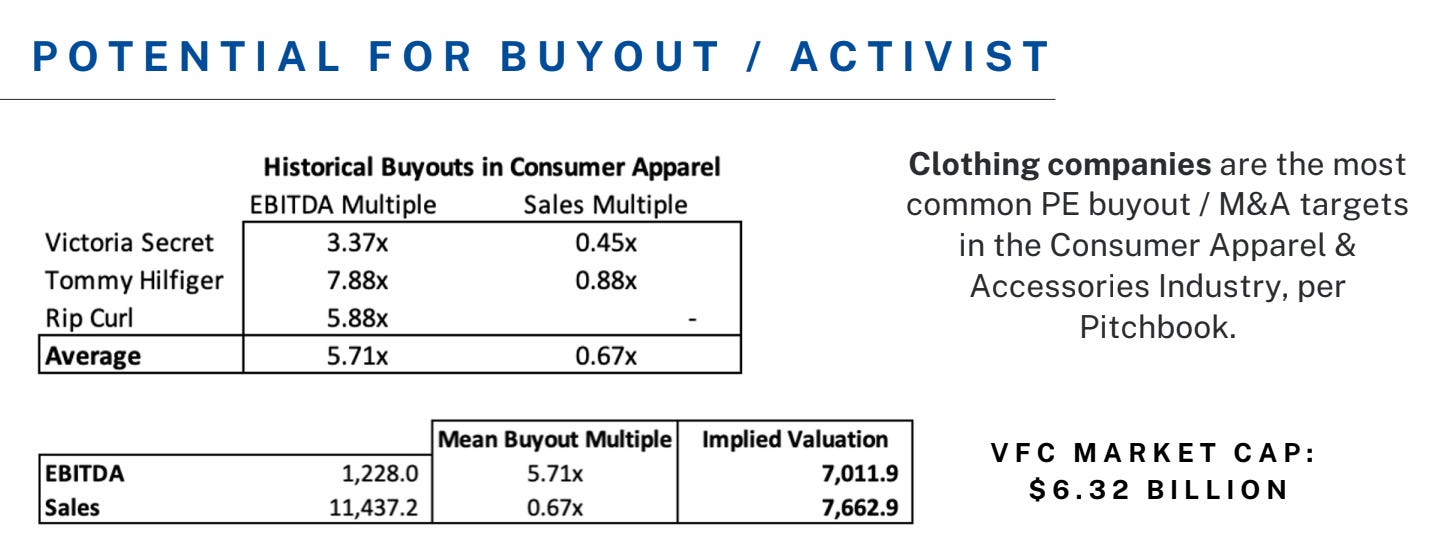

Looking at historical consumer apparel buyouts, VFC is already trading at a level below these buyout multiples. While this isn’t a precise measurement of undervaluation, it’s something to note.

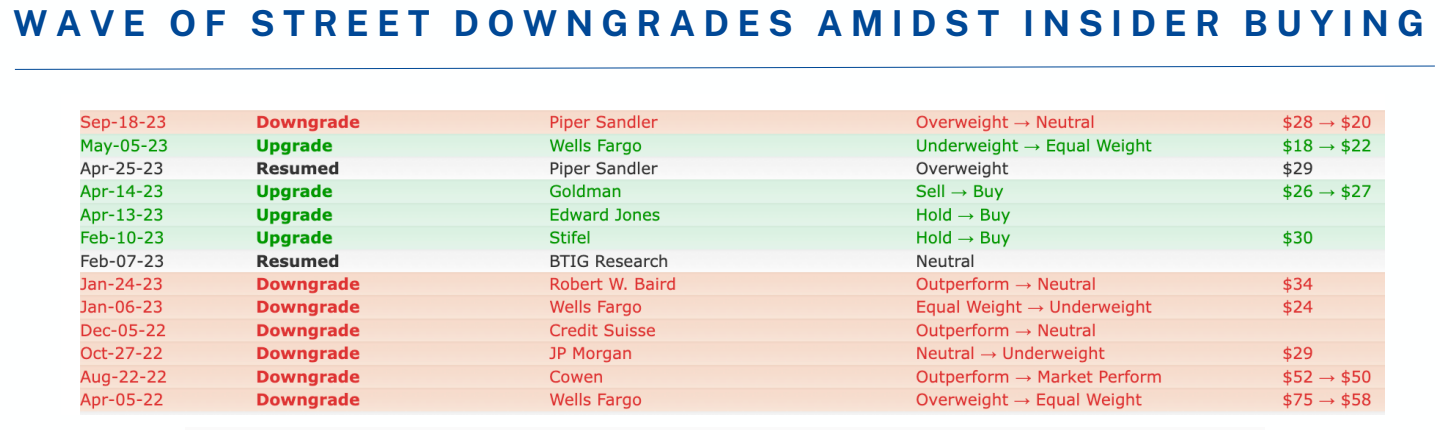

There has also been a wave of downgrades from Wall Street sell-side analysts despite massive insider buying, which is typically a good sign. Most notably, there were two insider buys on December 9th, the same day Steve Rendle exited as VF’s CEO.

The stock is obviously at quite a depressed level at the moment, so I created a reverse DCF model in order to figure out what the market may be pricing into the stock right now. My research led me to 3 core assumptions that I believe the market is pricing:

Consistent revenue decline over the next 5 years

Historical trough EBIT margins (only reached in 1996 and 2020) for the next 5 years

Double the capital expenditures over the next 5 years in order to repair and maintain VF’s brands

While the revenue decline and higher capital expenditure spend may be plausible, it seems a stretch to assume that EBIT margins will stay at such low levels for the next 5 years. VF Corp’s margins have been hammered by impairment charges related to the Supreme acquisition and excluding these impairment charges, VF’s EBIT margins are already back around 10%.

Long story short, the market is very pessimistic about the future of VF.

Valuation

Through the 3-statement DCF I built, there were some notable assumptions that I made.

Flat revenue growth

A slight decrease in gross margins

SG&A stays constant as a % of sales

Through these assumptions, I got a fair value per share of $37.70 and $20.60 from the perpetuity and EBITDA exit multiple methods. I then weighted the perpetuity method at 25% and the EBITDA exit method at 75% since the thesis for VF doesn’t necessarily rely on perpetual growth.

From there, I got a fair value per share of $24.88, representing over 50% upside from the current market price.

Potential Risks

I’ll start out by saying that this is a VERY RISKY INVESTMENT. The thesis for this company is one that is massively contingent on the new CEO who has no experience in the consumer apparel business.

There’s also a massive risk with the debt. Another risk is that management doesn’t take the debt seriously and continues to pay large dividends and buyback stock.

Inventory is another problem. Will the company be able to dump inventory to consumers with promotions while simultaneously not training the customer to wait for sales?

And then in general, the macro environment has not been friendly to consumer discretionary companies like VF Corp.

As always do your own research before considering an investment. This is strictly for educational and entertainment purposes ONLY.

Love the analysis and enjoyed reading it! Really appreciate the effort