🎓👨🏫 The Ultimate Guide to Student Loans

The Cost of Education: A Guide to Student Loans

Earning a college degree can be a great investment in your future, but it comes with a hefty price tag in the U.S. With the rising cost of tuition, room and board, and other expenses, many Americans don’t hesitate to take out loans to finance education. This can have a huge effect on finances long after graduation. Whether you’re a current or prospective student, or the parent of a current or prospective student, it’s important to understand how colleges and student loans work, as well as how to strategize paying them off quickly.

The good news is that you can shop around for schools to find one that fits you. Before we dive into loans, here’s a quick comparison between private and public colleges:

Private Colleges

Rely on tuition and donors for funding

More expensive

Smaller campuses with fewer students = smaller class sizes

Limited options for majors, so make sure what you want to study is offered!

Public Colleges

Funded by the government

Less expensive, especially if you’re a resident of the state (in-state tuition)

Larger campuses, more students = bigger classes

More options for majors

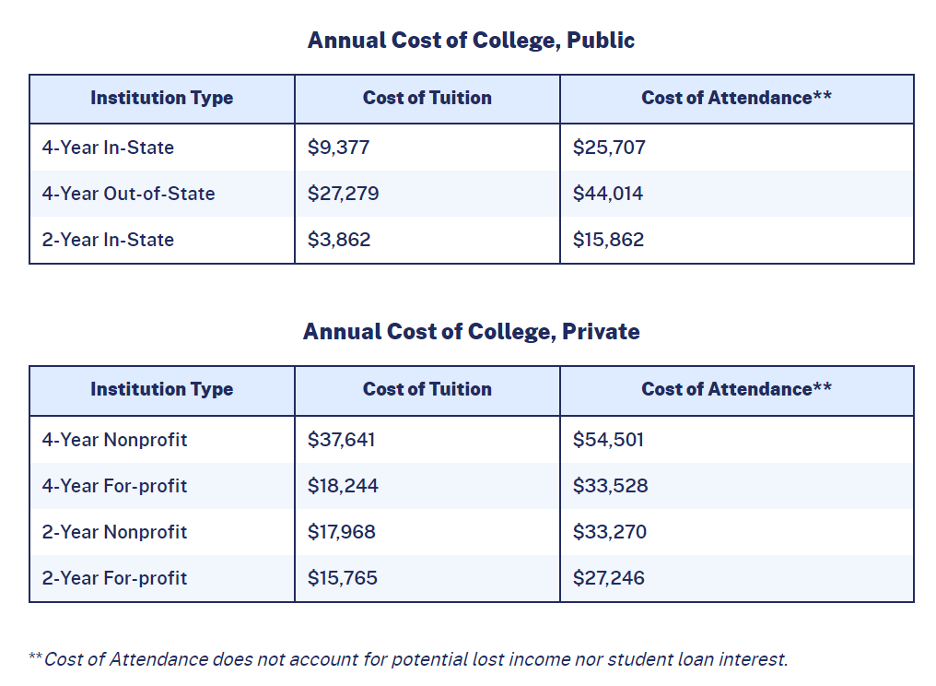

Take a look at this table to get a basic idea of the average cost of attending college in 2023. In-state public colleges are usually the most friendly to your wallet, so definitely consider them for a more affordable schooling option. Note that to be considered ‘in-state,’ the student usually has to reside within the state for 1 year prior to enrollment, but be sure to double-check these requirements with your school of choice.

A Note About Funding Education

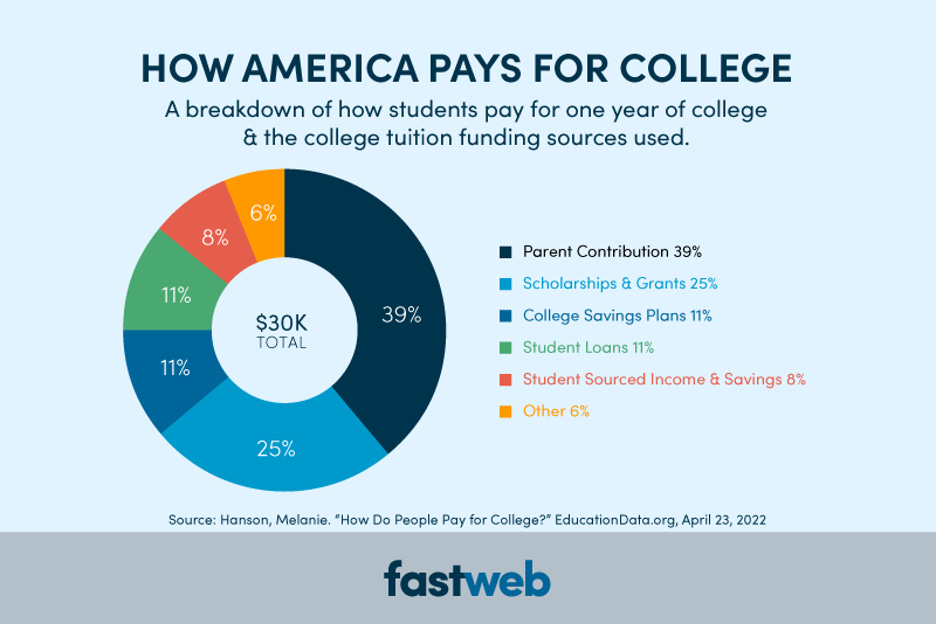

Ideally, student loans should make up part of your college payment, not all of it. Before taking out tons of student loans, look at all of your options through saving, earning scholarships, grants, etc. to help fund part of the tuition. Check out this sample breakdown of how you could divide up college funding, with student loans being a small piece of the pie.

How Student Loans Work

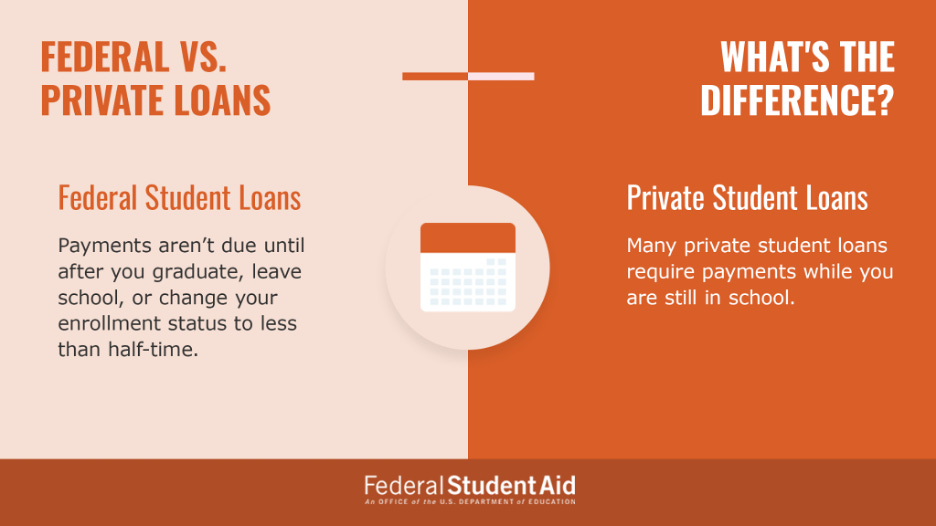

There are two kinds of student loans: federal and private. It’s important to have a solid understanding of both types of loans because they have very different sources, repayment options, and interest terms.

Here are some key differences between federal and private student loans:

Federal Loans

You have to apply for student aid using the FAFSA® form

Issued by the government

Most don’t require a credit check

Repayment term is usually 10 years

Fixed, low interest rates

Current rate is 4.99%

Flexible repayment options

May be forgiven if you meet certain requirements

There are four types of federal student loans:

Direct Subsidized: You have some time before you have to start paying these off. The government pays the interest on these loans while you’re in school and for six months after you graduate or drop below half-time enrollment status.

Direct Unsubsidized: Available to undergraduate and graduate students, regardless of financial need. Start paying these loans as soon as possible, because interest accrues while you’re still in school!

Direct PLUS: Available to graduate or professional students and parents of dependent undergraduate students. These require a credit check and have higher interest rates than other federal student loans.

Direct Consolidation: Allow you to combine multiple federal student loans into one loan with one monthly payment. The interest rate is based on the average of the interest rates of the loans you’re consolidating.

Private Loans

Issued by banks, credit unions, and other financial institutions

Require a credit check (your credit score determines your interest rate)

Variable, high interest rates

The rate can change over the term of your loan

Less flexible payment options

Repayment term ranges from 5-20 years

Usually not eligible for forgiveness; you're responsible for paying it back

Interest accrues on these as soon as you take them out, so start making payments as soon as possible!

Loan Repayment

Keep reading with a 7-day free trial

Subscribe to Hump 🐪 Days to keep reading this post and get 7 days of free access to the full post archives.