🏦👇 SVB Collapse: More Details Emerge

Happy Wednesday all,

It’s been a super eventful past week and today we’re explaining the Silicon Valley Bank collapse in our Hump Days Scoop.

In personal news, I’ve moved into a new place so you may see a new studio set in YouTube videos in the future. Here’s an angle that I like:

It’ll be cleaned up in the background, and I’ll add some plants and lighting as well 😂

Enjoy this week’s Hump Days!

- Humphrey, Rickie & Tim

Tweet of the Week

The Weekly Brief

U.S. Inflation Cooled in February as Fed Confronts Bank Failures (WSJ)

The consumer price index rose 6% in February from a year earlier, the smallest increase since September 2021 but still stubbornly high. Excluding volatile food and energy costs, the “core” inflation rose at a slower 5.5%. Economists view core prices as a better indicator of future inflation.

Why Does it Matter?

The Fed still has a ton of work left to do. Elevated inflation data, paired with strong labor/consumer spending data appeared to put the Fed in a position to consider a larger interest rate hike at the next meeting but the collapse of SVB could lead the central bank to move more cautiously to assess the state of the financial system.Saudi Aramco Reports Record Profit of $161.1B in 2022 (Reuters)

Saudi Aramco reported a record annual profit of $161.1B for 2022, up 46% from the previous year on higher energy prices, increased volumes sold, and improved margins for its refined products. To put it in perspective, Saudi Aramco made triple the amount that Exxon made. Many in the oil & gas industry reported record profits for the last year including BP, Shell, and Chevron.

Why Does it Matter?

It looks like a lot of companies are taking advantage of the fact that Inflation is higher, seeing it as an opportunity to keep their energy prices higher. In addressing concerns about national security, TikTok’s leadership discussed the possibility of separating from ByteDance through a sale or initial public offering (IPO). TikTok’s U.S. business is valued between $40B-$50B based on comparable competitors. A split would be considered a last resort which would only be pursued if national security officials disapprove of its existing proposal.

Why Does it Matter?

We had whispers of this in 2020 when Trump wanted to ban Tik Tok. The response would be for them to sell off their US-business unit. Either way, if this were to happen it's not going to happen that quickly - and will likely still be an ongoing debate for the 2024 election cycle. There is precedent for a ban on a foreign entity - most notably Huawei the cell phone maker, which was banned in 2019 from the US. You’ll Find This Interesting

$30M+ Wroth of Funkos are headed to the landfill after overestimating demand. Funko’s warehouses are filling up and the company decided that throwing them out would be cheaper than trying to sell them. Funko’s stock price fell off a cliff in the days following its press release.

Hump Days Scoop

Last week, in the span of 48 hours, we saw the 2nd and 3rd largest bank failures in the history of our global financial system. A lot has been spoken on the news since the collapse but there are still lots of gaps. Today, we try and fill in some of those gaps. Strap yourself in. It’s going to be a bumpy ride.

Why did SVB and Signature Bank Collapse?

The main talking point on social media and news outlets was that SVB and Signature Banks had a bank run where there was an influx of depositors wanting to withdraw all their money at once; and because of fractional reserve banking that only requires the bank to maintain at least 10% of the original deposit so it can loan out the other 90% and make money on it.

However, that only scratches the surface of the root cause and in the case of SVB, it was interest rate risk paired with liquidity risk that ultimately led to its downfall. During the startup/tech boom from 2019 to 2021, SVB, which mainly dealt with startup clientele, saw the rate that it was receiving deposits increase against the rate at which it could loan money to customers. SVB decided instead of having the money sit with no customers willing to take out loans, it would invest a large chunk into bonds in order to at least lock in a 1.5%-2% return on its money.

What we saw next was SVB needing to sell off a significant chunk of its bond portfolio in order to have enough money to fulfill all deposit requests, but because of the timing, it sold at a $1.8B loss. SVB then announced it would need to raise equity in order to make the difference which caused a major stir among VCs and startup founders rushing to withdraw their money before SVB went dry. Signature Bank, which is a big lender in the crypto industry, credited its downfall to SVB-generated panic.

Why did SVB need to sell at such a significant loss on its bond portfolio?

The bond market is significantly more complex than the stock market, and although it may seem like a simple concept, the bond market is much less transparent. When you buy bonds, you put up an amount of cash (say, $10,000), and for having put up that cash, you get a coupon every 6 months for a set percentage that you agreed upon when buying the bond. Simple stuff. But what many people overlook is that bonds are a tradeable asset. That means the value of the bond fluctuates in relation to broader interest rates. Why would I buy your $10,000 bond with a 2% coupon when I can buy a bond from the government with a 3.5% coupon? You’re going to need to make up that difference if you want me to buy your bond, and that is exactly what SVB had to do to have their bonds sell.

How did the government respond?

While many are calling it a bailout, the Federal Reserve, Treasury Department, and the FDIC made sure to clear up any misconceptions Sunday night. These regulators announced emergency measures that involved ensuring all depositors would be made whole. Stock and bondholders would not be protected through these measures (which means it does not constitute a bailout) and federal regulators said any losses to the government’s fund would be recovered in a special assessment on banks and that the U.S. taxpayers would not bear any losses.

What led up to this? Who’s at fault for this?

President Biden pointed fingers at the Trump administration for the collapse of SVB citing the repeal of measures put in place by the Obama administration to put tighter requirements on smaller banks.

Biden, in this case, is referring to Trump’s 2018 rollback of the 2010 law signed by Obama, widely known as Dodd-Frank. This law required banks with at least $50M in assets to maintain a certain level of capital and liquidity, and to file a “living will” plan every year that outlined their steps for a quick and orderly dissolution of assets if they were to fail.

The motivation for the 2018 rollback was to allow smaller banks to be more competitive and could be fairly described as bipartisan at the time.

Is the banking system safe? Is this going to spread to other parts of the world?

The fear among many in the startup community was that without their deposits in SVB, they would not be able to make payroll the following week or pay their creditors. You can see how far this spirals when you take into account all the parties involved. Company A fails to pay Company B for services they already performed, Company B contracted Company C to fulfill part of the work, and now, Company B can’t make payroll either.

This is why the government was so quick to ensure all depositors would be made whole. Acting as a backstop for SVB depositors was the government’s attempt at reassuring that the U.S. banking system is safe. What ensued next, was a flock of capital going to the big 4 banks in the U.S.: JP Morgan, Bank of America, Citigroup, and Wells Fargo.

As it currently stands, the impact of the SVB collapse does not seem to worry Eurozone supervisors because Eurozone banks are still well-funded and significantly more conservative than SVB. The European Central Bank did not see the need to hold an emergency meeting, signaling that they did not see the risk spreading to Europe.

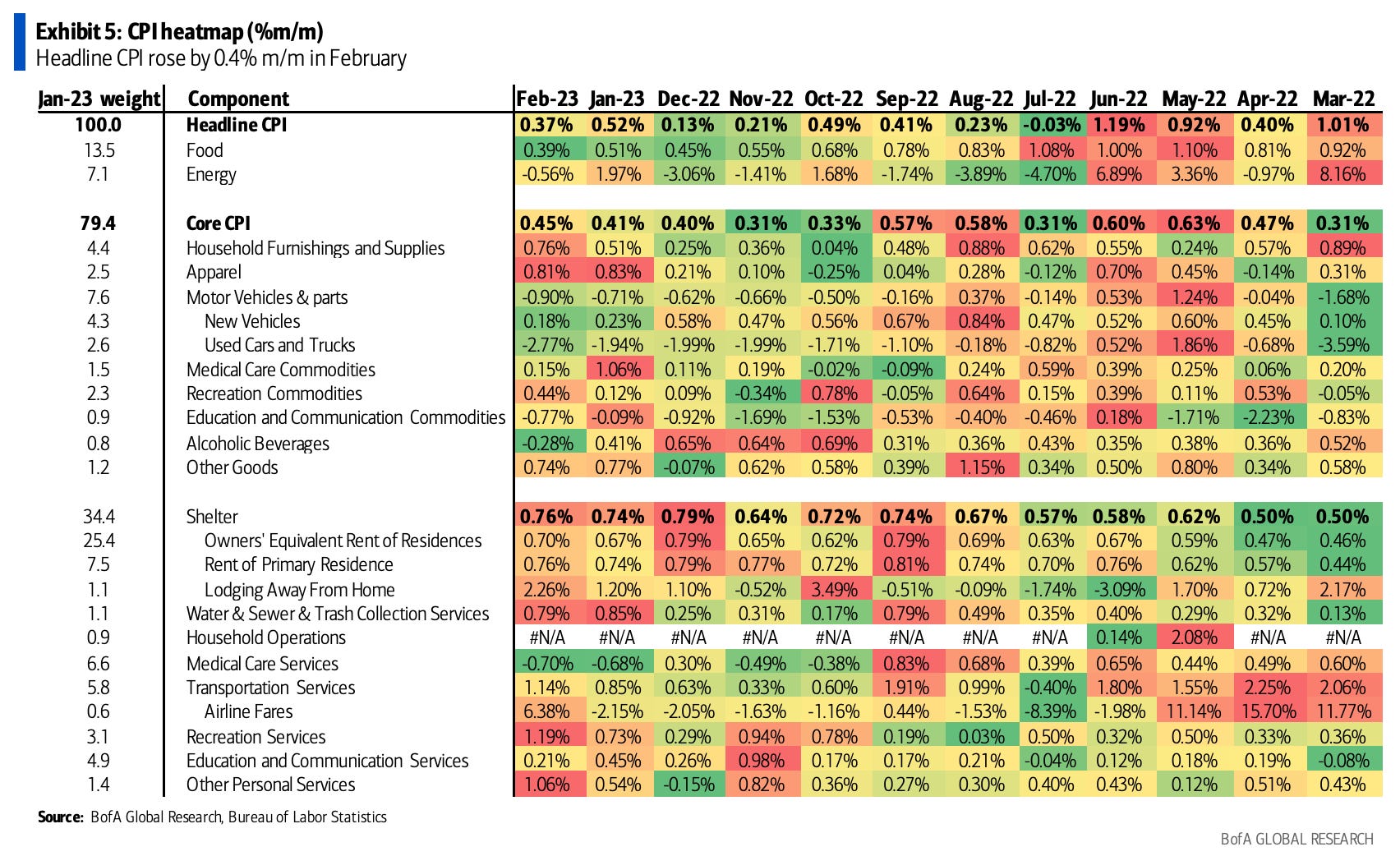

Chart of the Week

February’s inflation report came in line with Wall Street’s expectations.

Food prices rose by 0.4% MoM, slightly below expectations and energy prices fell by 0.6% MoM. However, core inflation increased by 0.45% MoM, driven particularly by shelter inflation. In fact, over 70% of inflation growth was due to shelter inflation.