💻📉 Software Stocks Stumble

Happy Sunday,

Markets are heading into the 2026 earnings season with valuations stretched and expectations high. Investors are becoming increasingly selective as the AI trade shows early signs of fatigue, software stocks stumble, and capital spending demands real returns.

At the same time, disinflation continues at a measured pace, offering policy relief without easing the cost-of-living burden for consumers. With geopolitics, policy uncertainty, and earnings guidance now carrying more weight than headline results, this season may prove decisive for the durability of the multi-year bull market.

- Humphrey & Rickie

Market Report

Global Markets Face a High Bar as 2026 Earnings Season Begins

Investors are entering the 2026 earnings season with the MSCI World Index trading at a lofty 20 times forward earnings, significantly above its 10-year median of 17.

This elevated valuation leaves little room for disappointment, especially as the AI trade begins to fracture. While Taiwan Semiconductor Manufacturing (TSMC) provided a boost with strong revenue guidance, investors are becoming increasingly discerning.

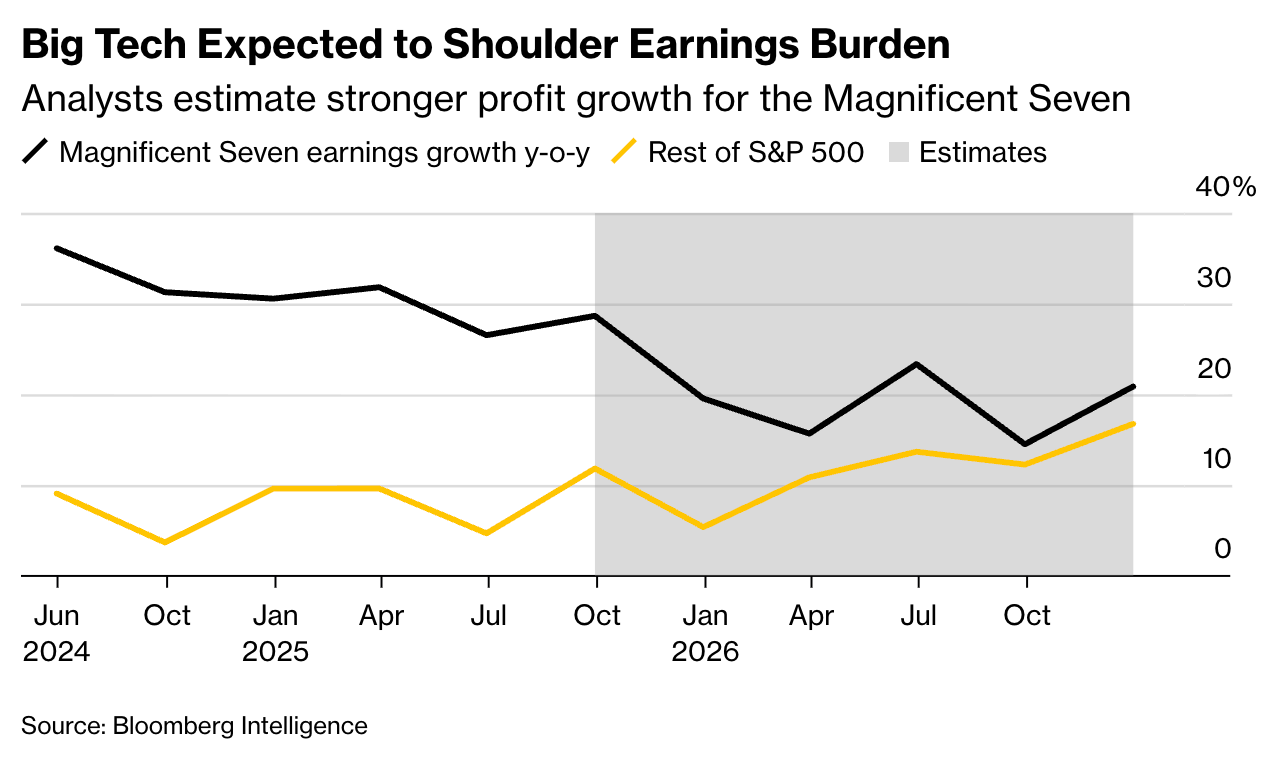

The Magnificent Seven are expected to shoulder a massive burden, with a projected 20% profit growth required to justify a staggering $530 billion in planned capital expenditures for 2026. Stocks that fail to demonstrate clear returns on these massive AI investments, such as Meta and Oracle, have already seen significant pullbacks, signaling that the “blank check” era for AI spending may be over.

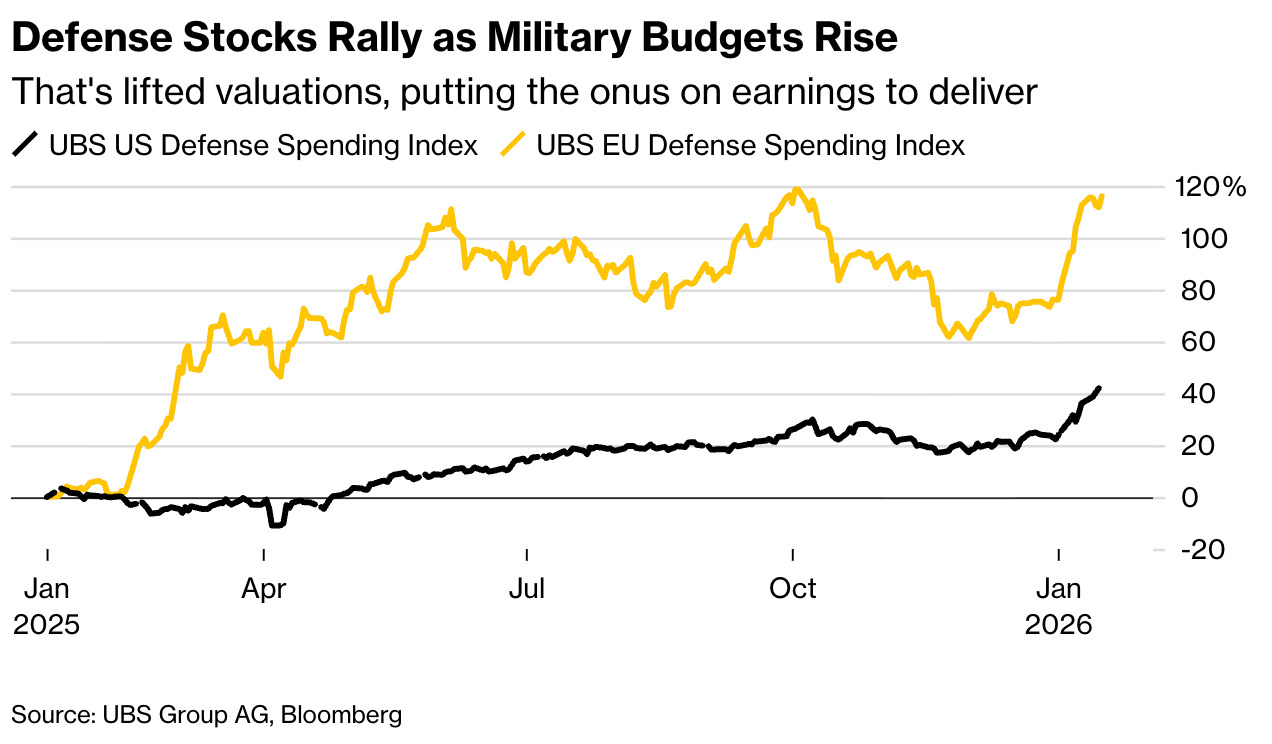

Beyond technology, the market’s focus is shifting toward geopolitical winners and the “old economy.” Geopolitical turmoil has sparked a defense sector boom, driving valuations for firms like Rheinmetall and Lockheed Martin to record highs of 29 to 32 times earnings.

However, corporate outlooks remain clouded by “policy chaos” from Washington, including a pivotal Supreme Court case on tariff legality and volatile oil markets following the US capture of Venezuela’s president.

While Europe and Asia anticipate a rebound with double-digit profit growth after a stagnant 2025, the persistence of trade jitters and a weakening labor market means that company guidance will likely be more critical than actual results in determining if the four-year bull run can continue.

The “Slow Grind” of Disinflation in 2025

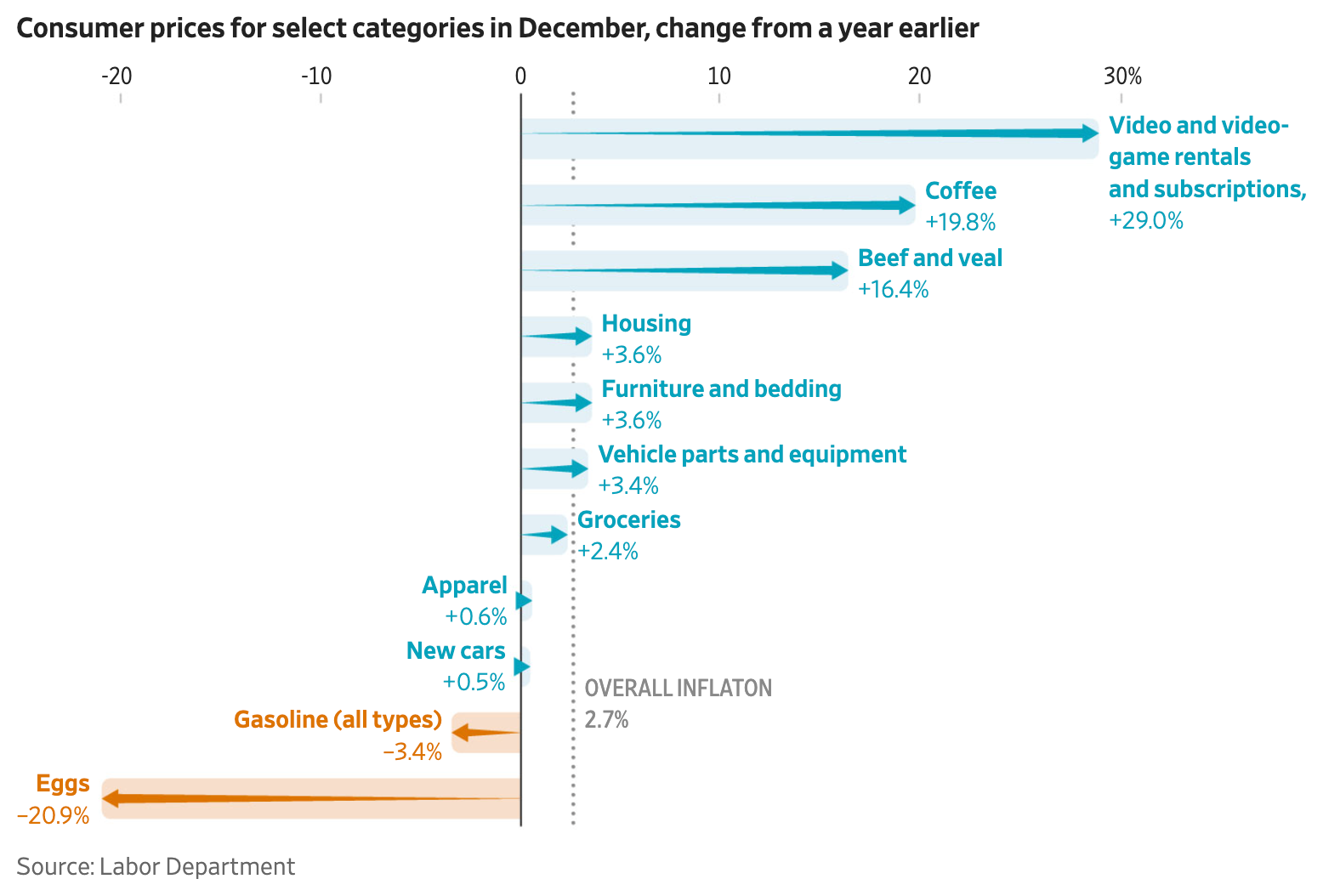

The US economy saw a notable deceleration in inflation throughout 2025, with the headline rate cooling to 2.7% in December and core inflation dropping to 2.6%.

While the Federal Reserve found some relief in these numbers, the “sticker shock” for consumers remains intense as price levels for essential goods remain far above pre-pandemic averages.

The year saw dramatic price divergences: while an easing of bird flu sent egg prices plunging 21% and gasoline costs ticked down 3.4%, other staples became significantly more expensive.

Coffee prices surged nearly 20% due to poor harvests and new tariffs, beef rose over 16%, and streaming service subscriptions skyrocketed by 29% as major platforms implemented aggressive price hikes.

While economists initially feared a sudden inflationary spike from trade protectionism, the impact manifested more gradually in categories like furniture and bedding (+3.6%) and vehicle parts (+3.4%).

Retailers absorbed some costs in competitive areas like apparel and toys, but the cumulative effect of high rents and record home prices has kept consumer sentiment depressed.

Turning to 2026, the primary challenge remains that while the rate of increase has slowed, the actual cost of living has yet to see a meaningful decline.

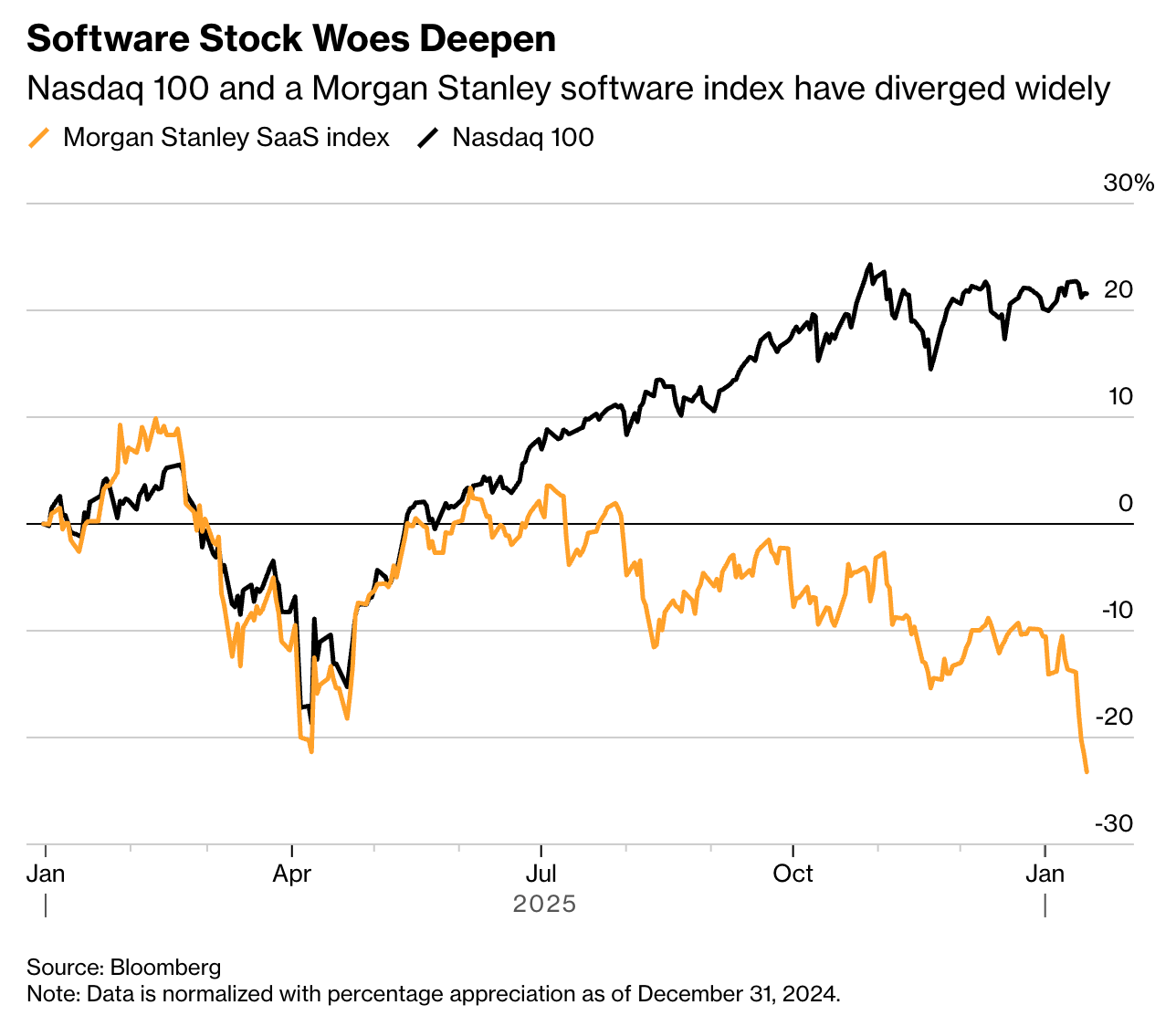

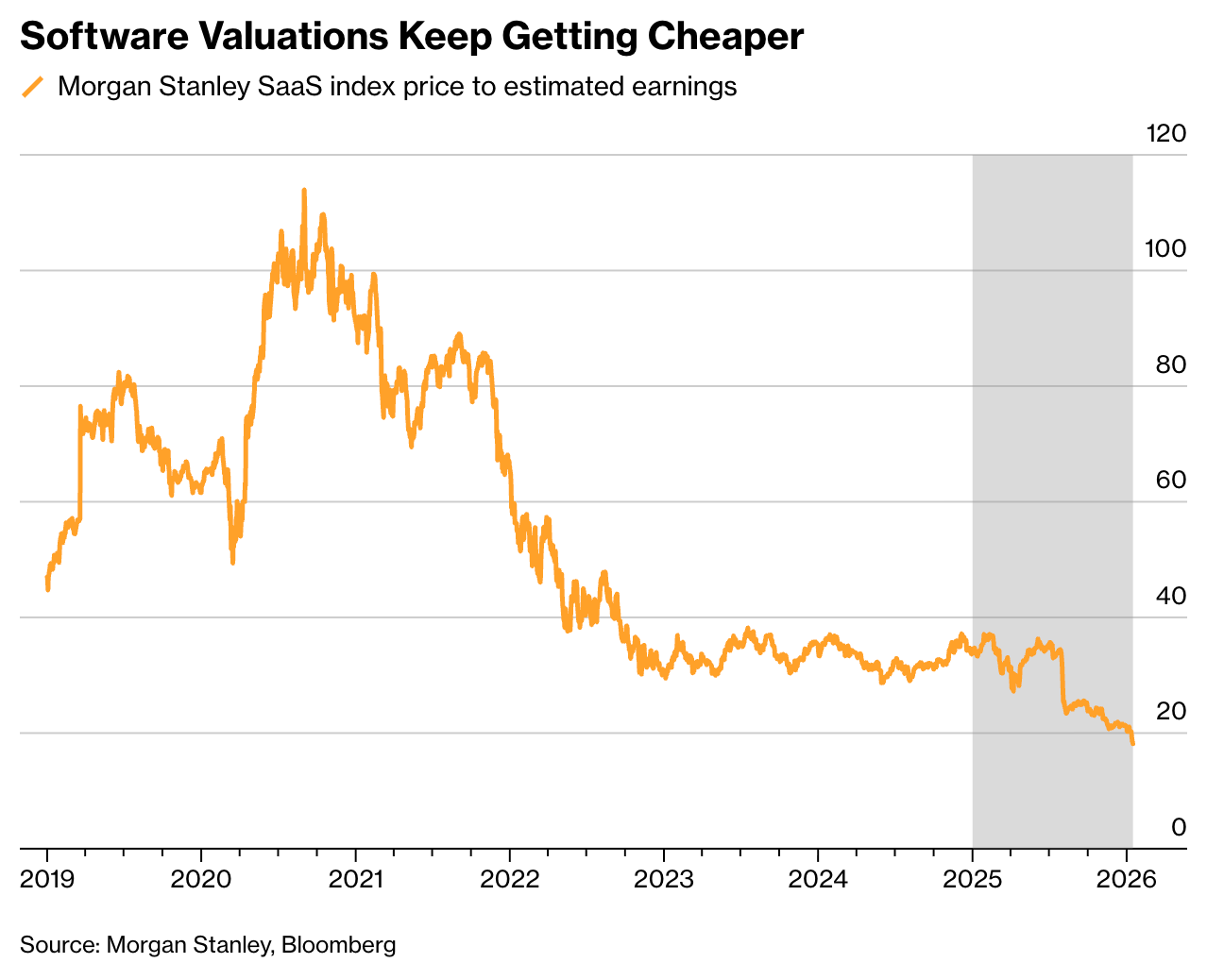

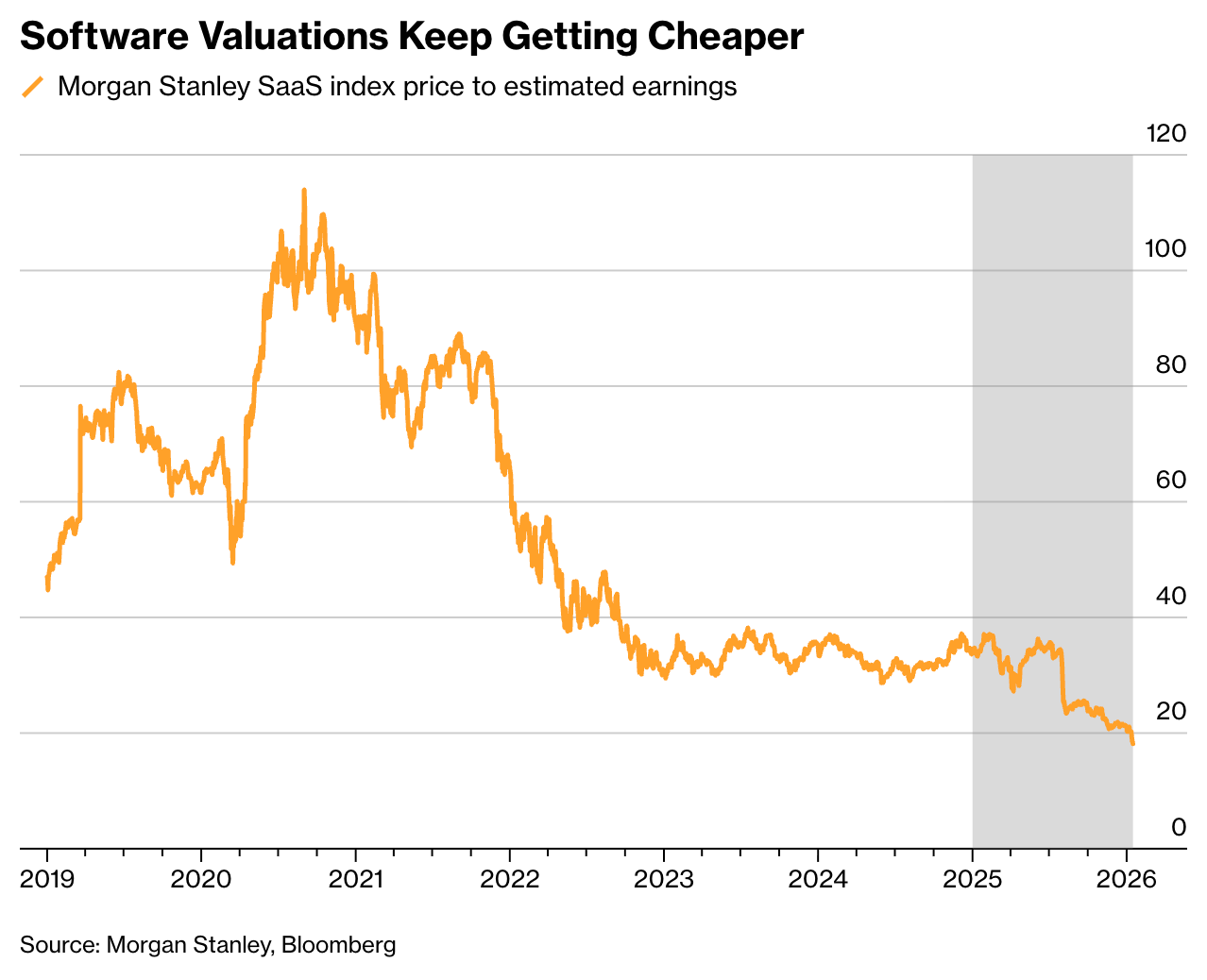

Software Stocks Stumble Amid AI Existential Crisis

The US software sector is off to its worst start in years, with a major basket of SaaS stocks plunging 15% in the first weeks of 2026. This selloff, which follows an 11% decline in 2025, was largely triggered by the release of Anthropic’s “Claude Cowork” AI tool.

The announcement reignited deep-seated investor fears that generative AI agents could disrupt or entirely replace incumbent platforms like Intuit, Adobe, and Salesforce.

Unlike the hardware sector, where companies like Nvidia enjoy clear revenue visibility from AI infrastructure spending, software makers have yet to prove their AI add-ons can meaningfully accelerate growth. As a result, the premium once paid for “stable” recurring revenue is evaporating as investors question whether subscription models can survive in an era of 24/7 AI agents.

Despite the grim start, the carnage has pushed software valuations to record lows, with the sector trading at just 18 times forward earnings, a fraction of its 55x decade-long average.

This valuation disconnect has divided Wall Street; while many institutional investors see no immediate catalyst for a rebound, firms like Goldman Sachs and Barclays argue the sector is “finally due for a break.”

Big Number

Overcome the Sunday Scaries

In Case You Missed It