🏦🔄 Raised Rates Again, Pivot Soon?

Welcome to the Sunday Primer,

We’re seeing rates raised across the board, savings interest rates are looking juicy, and we have a big week up ahead with the midterm elections. We have a video coming out on the channel on the interest rate environment so make sure to tick that notification bell if you haven’t already.

- Humphrey, Rickie & Tim

Market Report

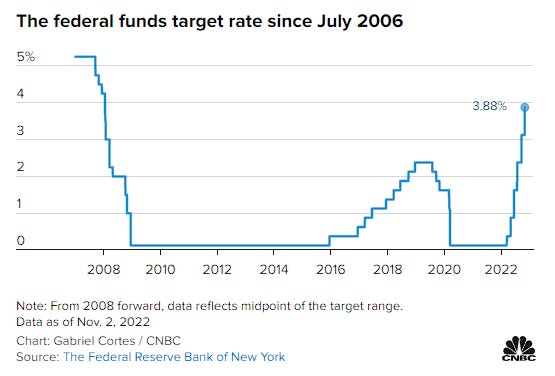

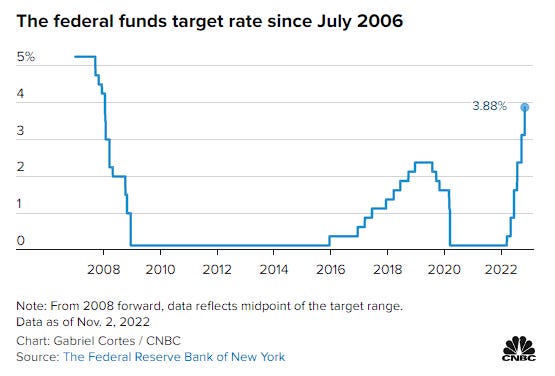

On Wednesday, the Federal Reserve raised interest rates by 0.75% to a range of 3.75%-4%, the highest level since January 2008. The move continued the most aggressive pace of monetary policy tightening since the early 1980s, the last time inflation ran this high. Going forward, expect a slower pace of rate hikes. Powell stated that policy lags complicate the ability of the Fed to read the results of its prior actions.

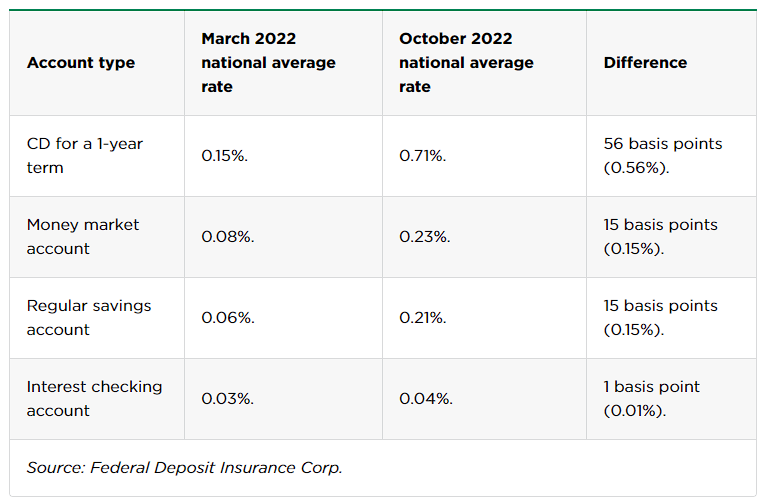

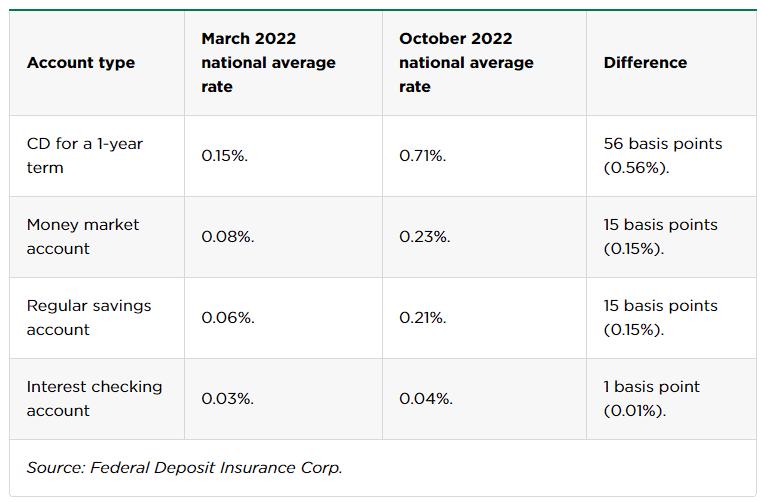

Here’s a look at four national average rates at banks for two months: in March — the month of the Fed’s first rate increase this year — and in October, after several Fed rate increases.

As a result, savings account APY’s have shot up at a lot of FinTech and online savings banks, here are some of the biggest rates we’re seeing. Below:

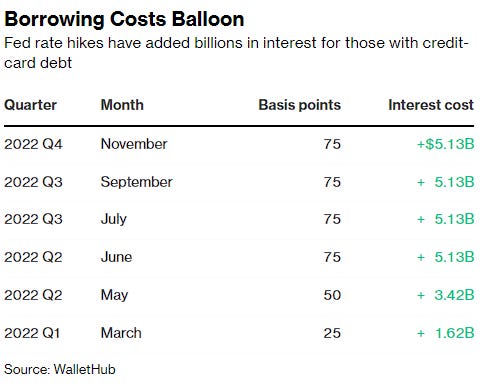

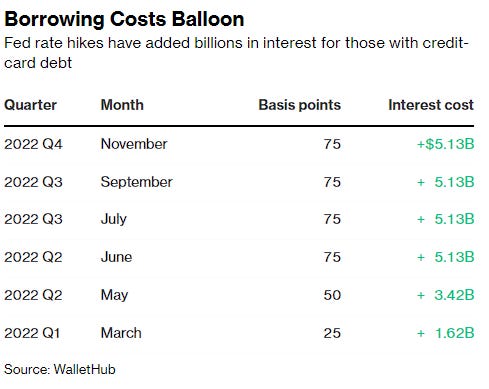

This recent hike will cost Americans with outstanding credit card debt more than $5 billion in additional interest over the next 12 months. The Fed’s aggressive rate increases this year have heaped about $25.6 billion in additional interest onto Americans’ yearly credit card bills. Since most credit cards have variable rates that are tied to the fed funds rate, people will probably see their interest rates go up overnight.

Forecast Ahead

October Inflation Report (Thursday, November 10th)

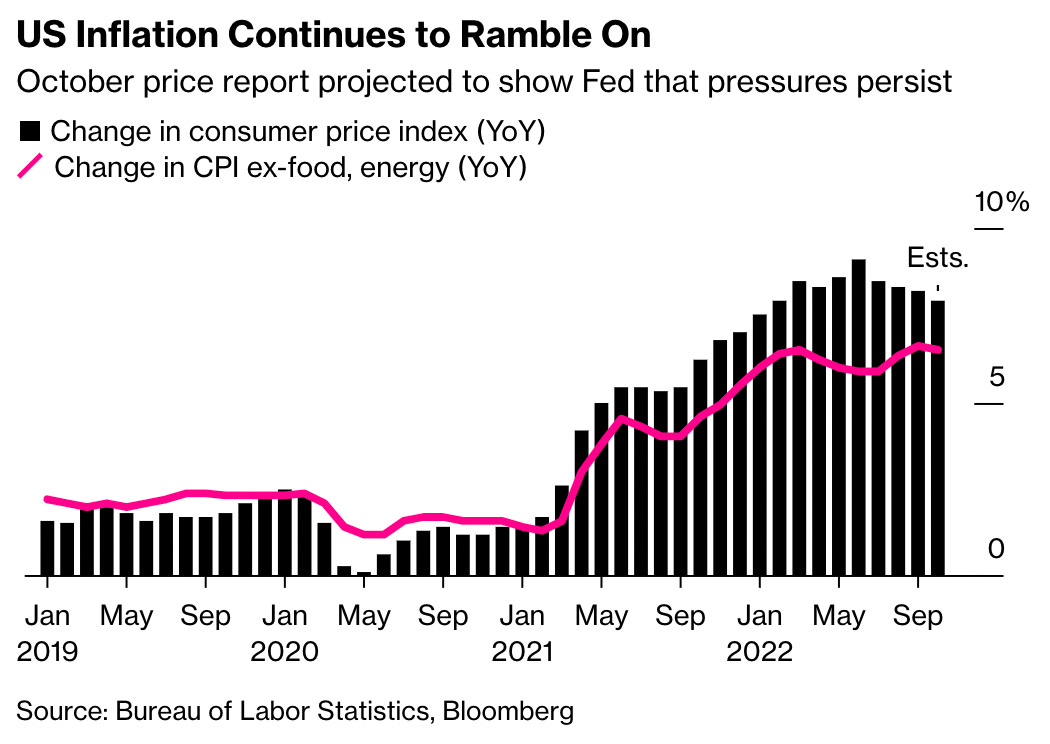

Analysts are expecting inflation to rise 0.7% over the past month, accelerating from a 0.4% increase in September. While the Federal Reserve has hinted that they were considering slowing the pace of rate hikes when they next gather in December, that will ultimately depend on inflation cools. Fed officials are already signaling that rates may peak at a higher level than previously projected.

U.S. Midterm Election (Tuesday, November 8th)

The fourth quarter and year after mid-term elections has historically been the market’s strongest stretch during the four-year presidential cycle.

COP27 (Throughout Week)

The UN’s annual climate summit kicks off this week as more than 100 heads of state and some 45,000 delegates eat to discuss the threats from war, an energy crisis, and the risk of a global recession.

Corporate Earnings (Throughout Week)

November 7th - Activision Blizzard (ATVI), BioNTech (BNTX), Diamondback Energy (FANG), Take-Two Interactive Software (TTWO), The Mosaic Company (MOS), Palantir Technologies (PLTR), SolarEdge Technologies (SEDG), Viatris Inc. (VTRS)

November 8th - The Walt Disney Company (DIS), Occidental Petroleum (OXY), Constellation Energy (CEG), DuPont (DD), Lucid Group (LCID), Fidelity National Financial (FNF), and Norwegian Cruise Line Holdings (NCLH)

November 9th - Coupang (CPNG), Rivian Automotive (RIVN), D.R. Horton (DHI), Roblox Corp. (RBLX), The Trade Desk (TTD)

November 10th - AstraZeneca (AZN), NIO Inc. (NIO), Toast Inc. (TOST), Celsius Holdings (CELH), U.S. Foods Corp. (USFD), Ralph Lauren (RL), Dillard’s Inc. (DDS), WeWork (WE)

What We Read Last Week

Stock Trader’s Guide to the US Midterm Elections (Bloomberg)

Raising Money on Wall Street Hasn’t Been This Hard in a Decade (WSJ)

French Study Finds No Inflation Profiteering in Food Sector (Bloomberg)

Elon Musk, Under Financial Pressure, Pushes to Make Money from Twitter (NYT)

Memes of the Week