🚙🔋 New 2023 EV Tax Credit, Barriers to Mass EV Adoption

Happy Hump Day everyone,

In this week’s featured story, we dive into the new electric vehicle tax credit brought forth by the Inflation Reduction Act that passed earlier this year. We dive into the specifics of how one qualifies for the new credit but also ask questions surrounding the reality of mass EV adoption, and the barrier that stands in their way.

Enjoy this week’s Hump Days!

- Humphrey, Rickie & Tim

Featured Story

The Inflation Reduction Act that passed in September earlier this year contained a number of measured aimed at incentivizing the purchase of domestically manufactured electric vehicles and increasing the adoption of EVs by making them more affordable. These new measures are slated to go into effect on January 1st, 2023, but how does one qualify for the tax credit? Which vehicles are allowed? Is the EV infrastructure within the U.S. reliable enough to handle the new influx in demand?

The main objective of the tax credit is surely on the demand side; make EVs more affordable by offering a $7,500 rebate on the purchase price. However, the new rules are also intended to impact the supply side by placing pressure on carmakers to reduce prices and produce their components within the U.S. The rules specify that no parts of the vehicle can come from “foreign entities of concern,” with this list including Iran and North Korea, but especially targeted towards disincentivizing production with parts from China (leader in the global supply of batteries) and Russia (abundance of raw materials such as nickel).

For those interested in the specifics of the credit, vehicles must meet three sets of eligibility requirements: MSRP caps (<$55k for cars, <$80k for SUVs/Trucks), buyer income caps (<$150k single/<$300k joint), and the final assembly provision. The provision involves the exclusion of the list of countries mentioned earlier but gets slightly more complex. The $7,500 tax credit is split equally into two parts. The first part is the Critical Minerals provision which requires a minimum percentage (which increases every year) of critical minerals must be extracted or processed by the U.S. or a free-trade partner country (Canada, EU, etc). The second half is the Battery Component provision that requires a minimum percentage (which increases every year) of battery components must be manufactured or assembled in North America.

Arguably, the largest roadblock to the mass adoption of EVs is the lack of commercial chargers around to power them. Suppliers of chargers and prospective EV adopters are at the question of chicken or egg. Drivers are not comfortable purchasing vehicles unless rapid charging is as easy and accessible as using a pump at a gas station. However, businesses interested in offering chargers say they can’t make money until more EVs are on the road. Rural states say some charging stations could operate at a loss for a decade or more.

With growing waiting lists for EVs from GM, Ford, and Tesla, the U.S. charging infrastructure must keep up to combat the “range anxiety” that EV drivers experience when traveling long distances. Currently, there are more than 145,000 places to refuel a gas-powered vehicle but only 11,600 points where an EV can charge quickly (20-60 min), according to Atlas Public Policy. The impact of the new tax credit will likely get more EVs on the road but will the infrastructure be there once those new cars get on the road? That remains to be seen.

Weekly News Roundup

U.S. Government to Backstop Mortgages Above $1M in High-Cost Areas (WSJ)

The federal government is set to backstop mortgages of more than $1M for the first time, starting in high-cost markets such as parts of California and New York. The maximum eligible for backing by Fannie Mae and Freddie Mac will rise to $1,089,300 in a few expensive markets, but for most of the country, loan limits will rise to $726,200. Mortgages within the limit generally come with lower closing costs and can require a smaller down payment. The increase reflects the rapid appreciation in home prices over the past few years.

HY: I think it also reflects the fact that there’s just more money in the economy.

Yield Curve Inversion Reaches New Extremes (WSJ)

Yields on longer-term U.S. Treasuries have fallen further below yields on short-term bonds than at any time in decades, a positive sign that investors believe the Fed is close to winning its inflation battle. Longer-term yields are generally higher than shorter-term yields but the current inversion of the yield curve means that investors are confident that short-term rates will be lower in the long term than in the near term. This is because investors think the Fed will need to slash borrowing costs to revive a flattening economy.

HY: Typically a yield inversion is an indicator a recession is coming. But this year, unlike others, seems to be different. Many experts agree that if the Fed continues to raise interest rates through 1st half of 2023 that it could cause a recession. However, I’m unsure if it will be a recession characterized by unemployment just yet. We’ll see.

U.S. Consumer Confidence at Four-Month Low; House Price Inflation Slows (Reuters)

Households are less keen to spend on big-ticket items over the next size months amid high inflation and rising borrowing costs, causing U.S. consumer confidence to slip to its four-month low in November. The decline in confidence was concentrated in the 55+ age group as well as among households with incomes <$50,000. Although, the survey showed that consumers remained upbeat about the labor market, which could limit some of the anticipated economic downturn. The labor market has remained resilient despite the Fed’s rate increases, helping to keep consumer spending and the overall economy afloat.

HY: We’ll keep an eye on this and probably make a video about it when the next CPI report drops in a couple weeks.

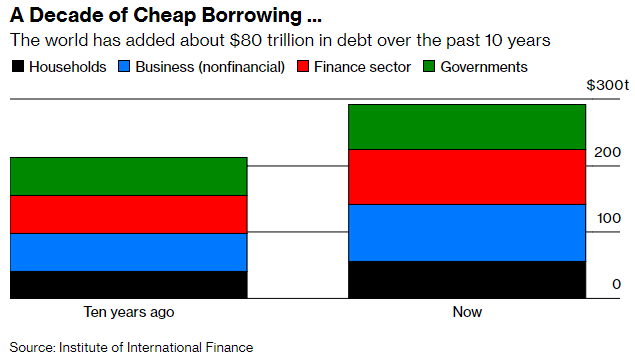

Chart of the Week

The total debt owed by households, businesses, and governments stands at $290 trillion, up by more than one-third from a decade ago.

Even though the world’s debt has declined from a pandemic-driven record early this year, many borrowers face an increase in their interest payments as the Federal Reserve and other central banks raise interest rates at the fastest pace in decades.