👨🏼💼 📉 Jerome Powell Signals Rate Cuts in 2024!

👨🏼💼 📉 Jerome Powell Signals Rate Cuts in 2024!

Happy Sunday!

I had a conversation with someone in the real estate industry last night and we both agreed that while interest rates may come down in Q1 or Q2 in 2024, that home prices may not come down. Homes may become more affordable (since the mortgage payment will be cheaper), but because of all the pent-up demand from the past year or so with elevated interest rates, we could see bidding wars still occur for homes in desirable cities and locations.

Anyway, let me know what you think of the housing market these days - are you trying to buy a home anytime soon? Are you priced out? Are you renting but hoping to save up for a down payment? Would love to get different perspectives. I’m also working on a video on the high costs of living that are starting to squeeze the middle class - and based on the data out there, it’s definitely going to be a topic of discussion during the 2024 Presidential Election.

Today’s Sunday edition is packed with good information for you, and we spent a lot of time on it - I hope you enjoy!

— Humphrey, Tim, & Rickie

P.S. I’ll be releasing a free community Discord server at the end of year / start of January, and it’s going to be a place where you can get together with like-minded individuals to discuss your finances, the news, and even ask me questions! Look out for that invite to the community in a couple short weeks!

Market Report

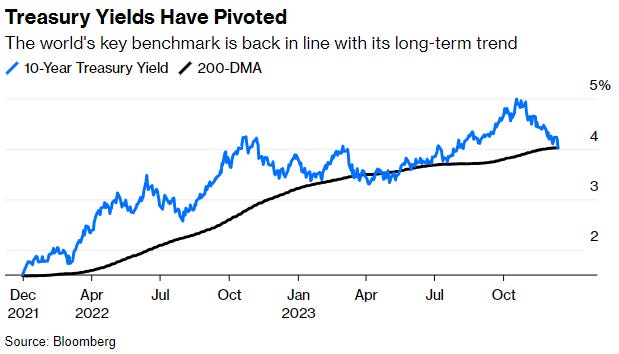

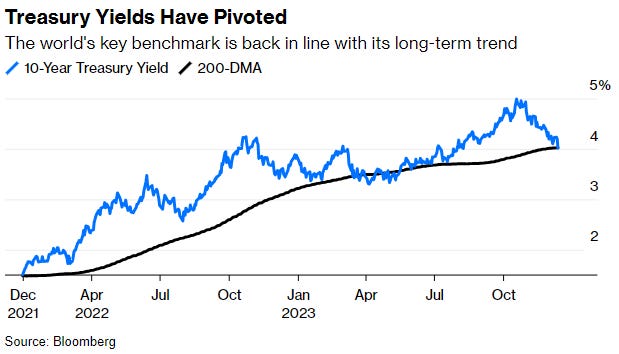

Federal Reserve's Strategic Shift: Future Rate Cuts Expected Ahead

What the Fed's rate policy pivot means for the economy (Axios)

Powell Pivots Toward a Happy New Year (Bloomberg)

Key Takeaways From Fed’s Rate Decision and Economic Forecasts (Bloomberg)

The Federal Reserve's latest interest-rate decision and economic forecasts, as announced on Wednesday, indicated a significant shift in its approach to monetary policy.

The Federal Open Market Committee (FOMC) unanimously decided to maintain the benchmark rate unchanged in the target range of 5.25%-5.5% for the third consecutive meeting.

This decision was widely expected.

However, the Fed's "dot plot" of rate projections revealed a broad range of estimates for potential rate cuts in the coming year.

The median projection is a 75 basis-point cut, with some officials anticipating smaller reductions while others expect more substantial cuts.

The FOMC also slightly softened its stance on future rate hikes, indicating a more cautious approach. Despite acknowledging that inflation has eased yet remains high, the Fed expressed optimism about economic growth, though slower than the robust pace seen in the third quarter.

The projections for inflation have been adjusted downwards for 2024 and 2025, and unemployment forecasts remain stable, suggesting growing confidence among Fed officials that they can control inflation without significant job losses.

The overarching message from the Federal Reserve indicates a nearing end to the aggressive fight against inflation, setting the stage for potential rate cuts in 2024.

This shift is significant for financial markets, businesses, and families, as it suggests a move away from policies aimed at slowing growth.

Additionally, the Fed's new outlook is buoyed by improvements in supply-side factors like resolving supply chain disruptions, increased labor force participation, and productivity gains, which are expected to help bring inflation closer to the Fed's 2% target.

This shift in the Fed's stance is reminiscent of its pivot towards a more hawkish stance in November 2021 but in the opposite direction, indicating a dovish pivot that has already started impacting the market.

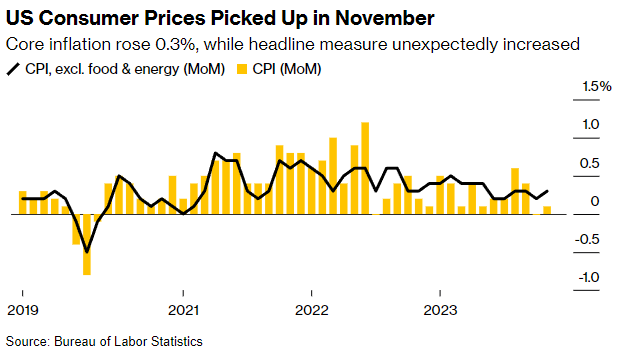

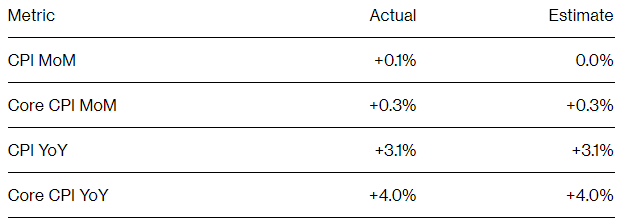

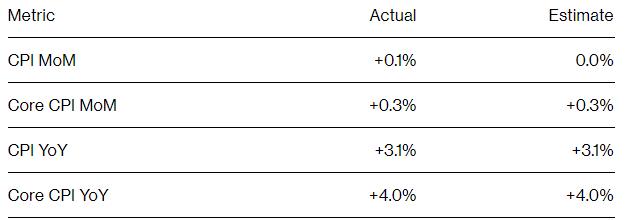

Inflation Picks Up Again in November

US Consumer Prices Pick Up in Bumpy Path Down for Inflation (Bloomberg)

In November, U.S. consumer prices witnessed an uptick, driven mainly by increases in housing and other service-sector costs.

The consumer price index (CPI) rose slightly from October, with core CPI, excluding food and energy, also accelerating, indicating persistent inflationary pressures.

Despite this, inflation is still on a general downward trajectory, with significant progress noted in the last six months. The data showed increases in rents, medical care, and motor vehicle insurance, coupled with a decrease in used-car prices.

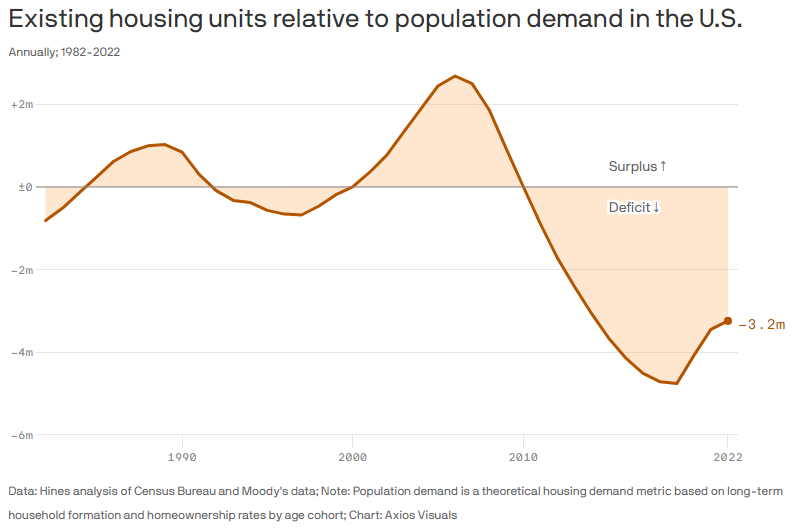

Analyzing America's Housing Shortage

America's housing shortage explained in one chart (Axios)

The United States is currently facing a significant housing shortage, estimated at around 3.2 million homes, or 2.5% of the existing inventory as of 2022.

This gap is a key factor driving high housing prices and reflects an inability to meet the rising number of households. The shortage is further compounded by the trend that most new constructions are high-end and unaffordable for many.

Major urban areas like New York and Los Angeles are experiencing the largest deficits, with only a few cities like New Orleans, Austin, and Nashville nearing equilibrium.

Despite an increase in apartment construction in recent years, overall housing starts have declined since the 2008 financial crisis.

This shortage poses a significant challenge for the upcoming wave of younger millennials and Gen Zers entering the homebuying market, with experts questioning the feasibility of meeting this demand due to high construction costs.

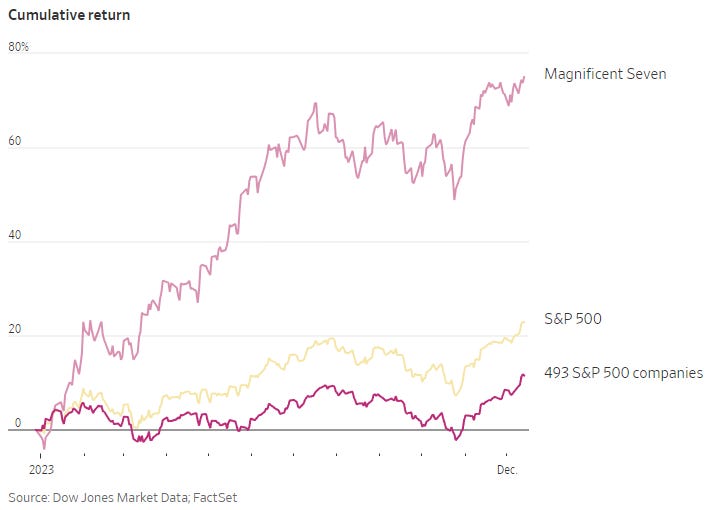

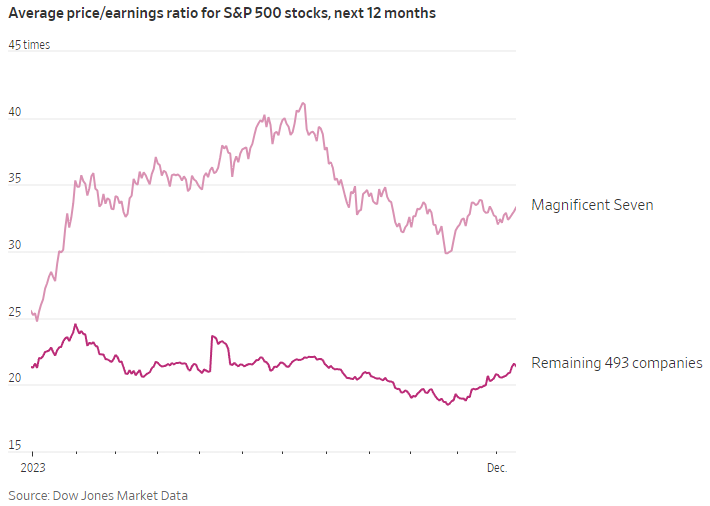

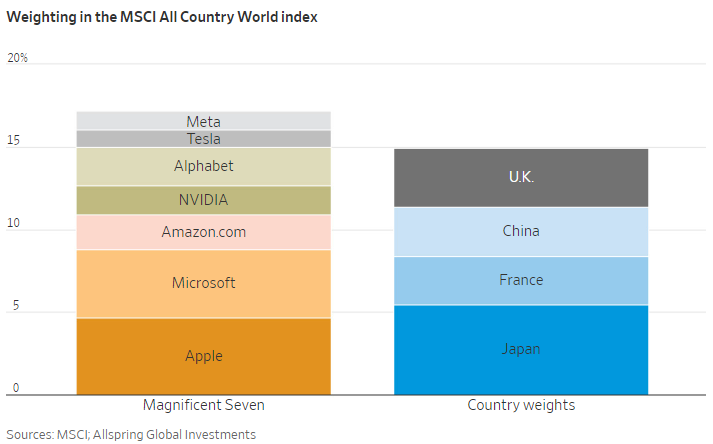

The Year of the Magnificent Seven

It’s the Magnificent Seven’s Market. The Other Stocks Are Just Living in It. (WSJ)

In 2023, big tech stocks, known as the Magnificent Seven (Apple, Microsoft, Alphabet, Amazon, Nvidia, Tesla, and Meta Platforms), significantly outperformed the market, surging 75% compared to a modest 12% rise in the other S&P 500 companies.

This group now represents about 30% of the S&P 500’s market value, highlighting their substantial influence in both the U.S. and global markets, as seen in the MSCI All Country World Index.

Despite concerns about market concentration and vulnerability to downturns, tech giants rebounded strongly from a 40% decline in 2022, driven by AI hype, favorable economic data, and easing inflation expectations.

Their high valuations compared to the broader market raise questions about sustainability, with some analysts predicting a shift towards other sectors in the future.

Forecast Ahead

Big Number: $6,054

The U.S. car market is facing a challenging period as high vehicle prices and increased interest rates have contributed to a significant rise in negative equity among car owners.

In November, the average amount owed beyond the car's value reached $6,054, the highest since April 2020, according to Edmunds.com.

This situation is exacerbated by longer loan terms and lower down payments, making it difficult for owners to build equity in their vehicles.

The used car market, which saw a spike in values during the pandemic due to supply chain issues and stimulus spending, has since experienced a sharp decline, further complicating the issue for car owners.

Overcome the Sunday Scaries

Memes of the Week