👨🔧 If I Started From Scratch, Here's How I'd Invest + Sunday Primer

Happy Sunday all,

We are close to 2023 being 66%, or two thirds of the way done already. Which is insane because I feel like New Years Day was just a few weeks ago even though it wasn’t.

In last Wednesday’s YouTube video, I distilled 8 key lessons that I’ve learned along the way of creating a stock portfolio. The TL;DR version is here:

Start a Roth IRA Earlier: I started mine at age 26, but the earlier you start the faster you can compound your wealth. The upside here is that all gains are tax free - so you should be aggressive when you’re younger.

Matching Holdings to Risk Profile: when I started out, I just copy/pasted a portfolio I found on Google. I recommend taking a risk questionnaire and then matching your investments to that risk profile.

Find Your Investing Style: part of this has to do with figuring out your time horizon and the goals you are investing for. By understanding your goals - choosing investments becomes easier.

Choose the right account: whether its a 401k, 403b, taxable brokerage account, IRA, or even a 529 plan - understand the pros/cons of each and invest accordingly.

Contribute more to retirement: the average American contributes about 6-8% of their paycheck to retirement, aim for 15%.

Find low fee funds: within your retirement plans, fees can be a killer long-term, so it’s important to find low expense ratios that are still well diversified.

Diversification: if you’re a passive investor - diversify. If you’re more active and understand your investments: diversification can be overrated. Just listen to Warren Buffett.

Tailoring your investments: lastly, there’s a resource matrix I created for my video that can help you understand the type of investments you should generally be looking at depending on your age and risk. It’s in the video - so check it out!

Have a great Sunday all!

— Humphrey, Tim, & Rickie

Economic Report

Consumers in the U.S. have been rapidly depleting the over $2 trillion in extra cash they saved during the pandemic, enabling continued spending even amid rising inflation and interest rates. But as this cash buffer fades away, there’s a growing concern that the economy is sitting on shaky ground.

Economists are still split on the economic possibilities. While some anticipate a recession due to pressures such as the restart of student loan payments and high costs of borrowing, others are more hopeful, referencing strong income growth and a resilient job market.

Recent data has shown strong US retail sales, with major consumer companies like Walmart, Target, and Home Depot reporting strong profits. Yet, there are warning signs, especially among lower-income households, with increasing reliance on credit cards and rising delinquencies on auto loans and credit cards.

Higher-income households aren’t immune either. Despite traditionally enjoying more economic stability than most households, those in the higher income bracket (earning over $125K) have seen softer year-over-year growth in after-tax wages, according to Bank of America.

While the trend of slowed income growth for this group has continued, lower- and middle-income households have maintained a steady after-tax wage growth of around 2-3% YoY, mirroring 2019 levels. In addition, even though the overall unemployment rate is still quite low at 3.5% in July, data indicates that higher-income earners are facing unemployment at a rate roughly three times faster than their lower-income peers.

Market Update

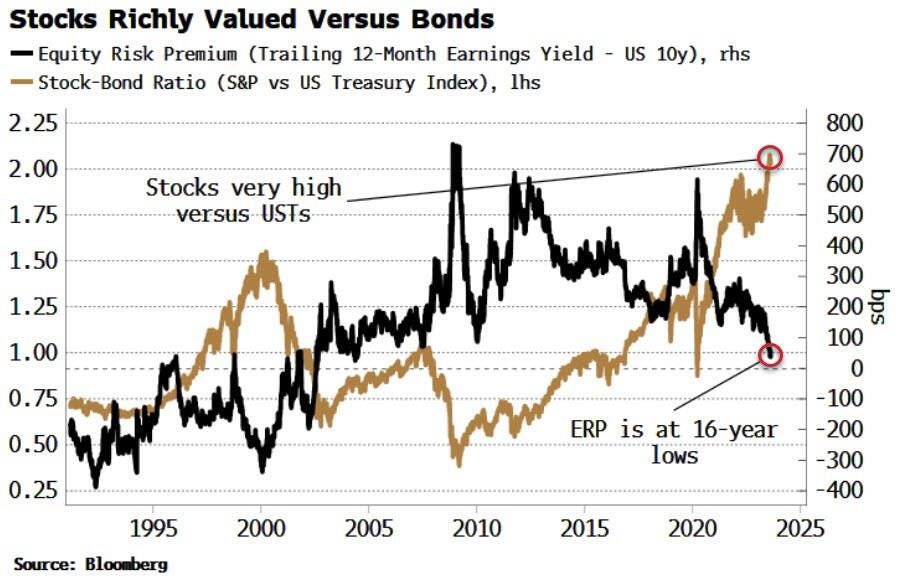

An interesting metric to follow has been the stock-bond ratio and the equity risk premium priced into the market.

When the stock-bond ratio increases, it suggests a preference for higher-risk and potentially higher-reward stocks, while a declining ratio indicates a tilt toward the safety of bonds.

The equity risk premium (ERP) quantifies the additional return investors expect for taking on the additional risk of stocks compared to the safety of bonds. A higher ERP suggests that investors require higher potential returns to invest in stocks, implying the many potential risks in the stock market, while a lower ERP indicates stronger investor confidence or lower expected returns from stocks relative to bonds.

Right now, the stock-bond ratio is currently elevated, suggesting a potential mean reversion to come, where stocks might underperform bonds. Meanwhile, the ERP has dropped to over 15-year lows, suggesting that investors aren't demanding as much extra return for the additional risk of holding stocks.

Robo-taxi Scrutiny in SF…

Cruise, GM's autonomous vehicle business, has been directed by the California DMV to cut its robotaxi fleet in San Francisco by 50% following a collision with a fire truck.

The agency is probing "recent concerning incidents" with Cruise vehicles and has mandated the company to limit its operations to 50 autonomous cars during the day and 150 at night until the investigation concludes. Although Cruise has faced various setbacks, including 10 of its driverless cars reportedly stalling, it remains committed to safety and expressed its intent to cooperate with the DMV.

Cruise was granted permission by the California Public Utilities Commission to expand commercial operations in San Francisco, allowing it to operate 24/7 and start charging for rides. This approval is now under renewed scrutiny after the accident. San Francisco City Attorney has petitioned the CPUC to halt Cruise and Waymo's charging plans for robotaxi services in the city.

In the past week, Cruise has had at least 10 of its driverless cars reportedly stalling and blocking traffic.

Forecast Ahead

Big Number: 1,700%

Overcome the Sunday Scaries

Memes of the Week

In Case You Missed It

Partnerships

If you are a brand looking to reach thousands of business leaders and investors through our two weekly newsletters, we would love to hear from you!