🏡💰 Household Debt Hits Record in 2022, What Next?

Happy Wednesday Friends,

We are well past 12,000 readers now on Hump Days, thank you for being here - incredibly grateful to have you. Moving forward, we’re planning to broaden the YouTube channel into more “outside of the box” topics on business, finance, economics, etc - so be on the lookout for more deep dives into those topics.

My other goal for the first half of this year is to interview some heavy hitters in the tech/finance/business/entrepreneurship space. Securing these interviews is difficult but I believe longer form (30-60 minute interviews) will include a lot of lessons and takeaways from successful people that we can all apply to our daily lives.

Finally, we filmed a thorough video with a Cookie Store owner last week - the owner brings in $140,000 a month in revenue - and takes home $28,000 a month working 25 hours a week. He was completely transparent with all his numbers which was refreshing and should give you some insight into how hard starting a food-based business is. Even though he works 25 hours a week now, it wasn’t always that way - in fact, he’s been in business for 6+ years and the early days were tough, to say the least. The video drops in a week or two - will update you when it’s out.

Enjoy this week’s Hump Days!

- Humphrey, Rickie & Tim

Tweet of the Week

The Weekly Brief

Canada’s Inflation Slows to 5.9% in January, Making Rate Pause More Likely (Reuters)

Canada’s annual inflation eased more than expected in January to 5.9% which should allow the Bank of Canada to keep interest rates steady at its next meeting while it lets previous rate hikes sink in. The Bank of Canada became the first major central bank to say it would hold off on further rate hikes as long as prices eased in line with its forecast. It expects inflation to slow to about 3% by the middle of 2023, and to come down to its 2% target next year.

Why Does it Matter?

The new figures show prices coming down faster in Canada than in the U.S., where inflation gained 6.4% in January. Bank of Canada's Deputy Governor said its policy-setting path can diverge from central banks in other countries as long as inflation is brought down to target. It looks as though Canada is in a more comfortable inflation environment to pause hikes at least temporarily.Law Firms Saw Deepening Decline in Client Demand at the end of 2022 (Reuters)

U.S. law firms ended 2022 seeing a worsening drop in client demand, declining productivity, and rising expenses. Demand for legal services fell 3.9% while productivity fell more than 7% year-over-year. Demand fell steeply in M&A work (down almost 17%), followed by real estate, bankruptcy, and tax practices.

Why Does it Matter?

It seemed as though layoffs were concentrated within tech but have now spread to the legal industry. It'll be key to keep an eye on the industry and to see if the decline in productivity spreads to other industries. Law firm finances were hit hard in 2020, saw record profits in 2021, and then a challenging 2022 after learning there was not enough work to occupy the lawyers they raced to hire in 2021.Retail Sales Jump 3% in January, Smashing Expectations Despite Inflation Increase (CNBC)

Sales at retailers burst through analyst predictions despite rising inflation pressure. Retail sales for the month increased by 3%, beating the forecast of 1.9%. Foodservice and drinking places surged by 7.2%, leading all major categories, followed by motor vehicles & parts dealers, and furniture. No categories saw a decline. Markets moved lower after the news.

Why Does it Matter?

The retail reports along with the monthly reports on industrial production and jobs came in better than expected and signal growth in economic activity to start off 2023. The Fed will take this into account when making decisions on interest rate hikes for the first half of the year. You’ll Find This Interesting

Ten companies that went public in 2020-2021 have gone back and went private, including Casper Sleep, McAfee, and F45 Training Holdings. Many of these companies are selling their shares at a loss. Grill maker Weber IPO’d at $14/share in mid-2021 and then agreed to go private in late-2022 for $8.05 a share. Others are expected to follow in the coming months.

Hump Days Scoop

The U.S. household debt hit a record 16.9T in Q4 2022 with credit card balances swelling at record rates. What’s going on? What does this all mean? What happens next? Let’s fill you in on what you need to know.

What makes up U.S. household debt and where are we seeing the increase?

U.S. household debt is largely split between mortgage debt, student debt, auto debt, and credit card debt. Much of the $394B increase is concentrated in mortgage debt making up more than half of the increase. The rise in mortgage debt can be attributed to the U.S. central bank raising its benchmark interest rate from near zero last March to more than 4% by the end of December. The interest rate hikes helped to cool a hot housing market but left those with floating-rate mortgages with climbing interest payments.

What is the area of most concern as it pertains to U.S. household debt?

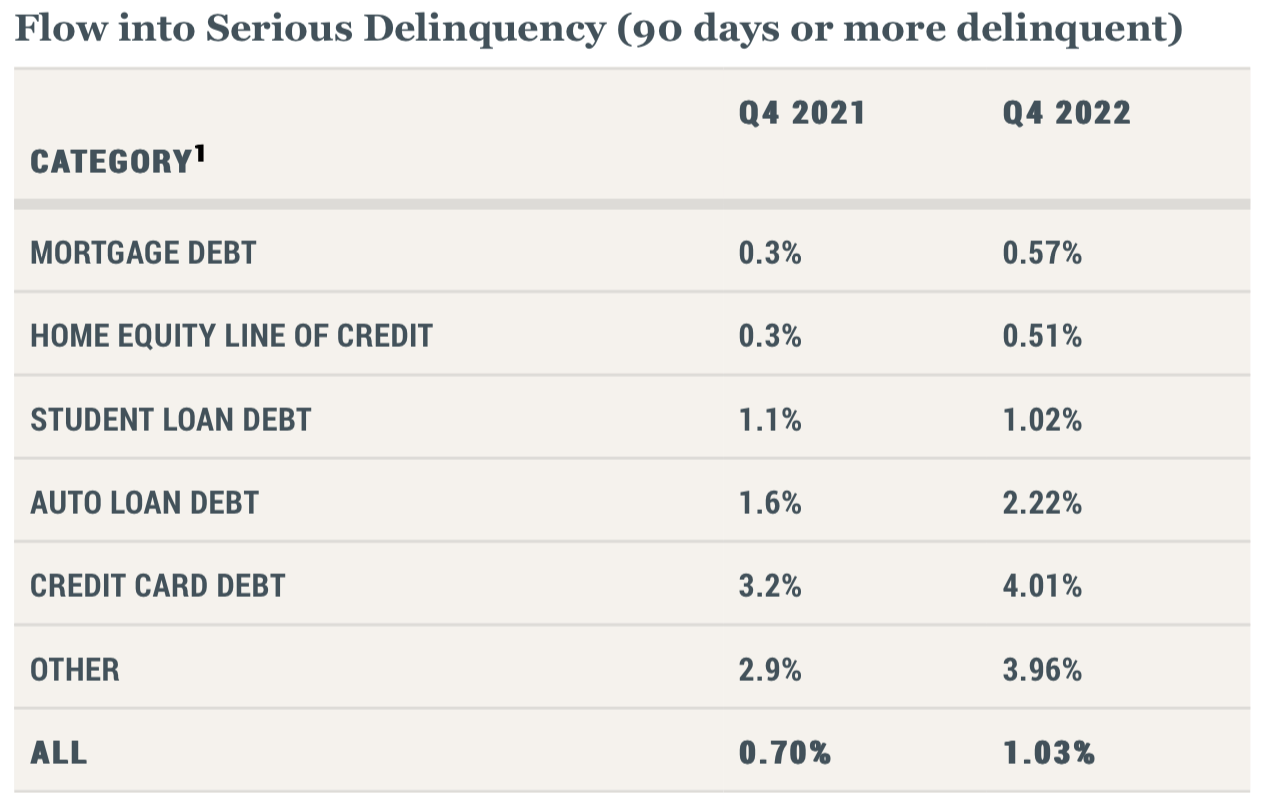

It is hard to pinpoint a singular point of most concern but we can start with how household debt translates into serious late payments by 90 days or more.

The chart above is straight from the Federal Reserve Bank of New York and it shows that serious delinquencies have increased nearly across the board. An area that many experts are concerned about is credit card debt because along with rising delinquencies, we’re seeing total credit card debt hit a record high of $986B, up $61B in Q4 alone.

Credit card debt and delinquencies are up. So what?

Something to note here is that even though credit card debt and delinquencies are up, both figures actually fell as a result of the pandemic. This increase actually marks a return to the pre-pandemic normal. However, the economic environment has changed significantly between then and now. For starters, while total credit card debt has returned to normal, it has gotten increasingly expensive to carry that debt. A year ago, the average credit card interest rate was ~18%. Over the last three months of 2022, that rate has jumped to 21.6% following the Fed’s aggressive series of rate hikes. As mortgage and auto-loan payments have increased across the board due to the interest rate environment, consumers are prioritizing keeping their homes and cars instead of paying off their credit card balances.

The increase in credit card interest rates and the subsequent rise in delinquencies is merely a symptom of what may be a larger issue at hand. What we could be seeing is that delinquencies are currently being propped up by a strong labor market. As long as people are employed, households are better able to make bill payments but as more people become unemployed, we may see a further rise in delinquencies on an already record amount of credit card debt. Currently, the unemployment rate is at a 53-year low. If delinquencies shoot up after unemployment goes up, that will indicate a serious, longer-term problem.

What We’ve Been Reading

Markets

Economy

Government

Stablecoins Attract Scrutiny in SEC’s Drive to Control Crypto (WSJ)

Biden Makes Show of Unity in Meeting with Eastern European Leaders in Poland (WSJ)

World

Putin Pulls Back From Last Remaining Nuclear Arms Control Pact with the U.S. (CNN)

Four-day Week Liked by U.K. Employers in World’s Largest Trial (Reuters)

Chart of the Week

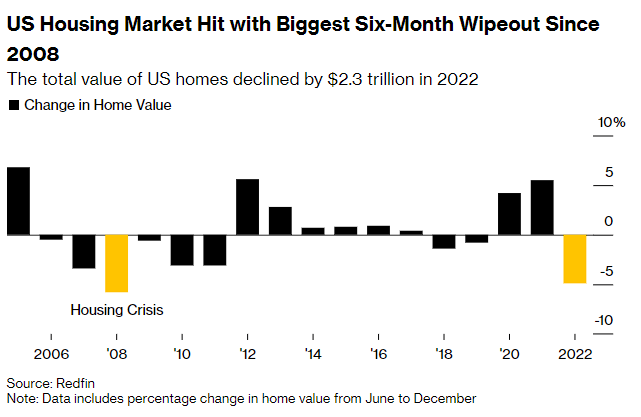

The U.S. housing market has experienced its largest decline in value since the 2008 housing crisis. The total value of US homes dropped by $2.3 trillion, or 4.9%, in the second half of 2022, after peaking at $47.7 trillion in June. The decline was attributed to the end of the pandemic housing boom and the more than doubling of mortgage rates last year.

The decline in home values has affected homebuyers, who were already facing record-high prices. However, with less competition in the market, the median U.S. home sale price has decreased to $383,249 as of last month, down from a peak of $433,133 in May.