💣🏦 Dealing with the Fallout of SVB

Happy Sunday,

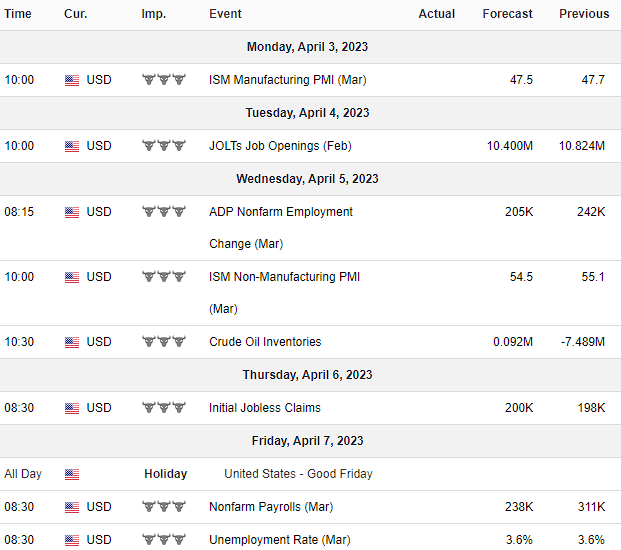

Quick reminder that the stock markets will be closed this coming Friday for Good Friday - April 7th.

In today’s newsletter we dive a bit deeper into the fallout from Silicon Valley Bank and also show you how April has historically performed for the market.

A question I get all the time is “how does the market keep going up over time?” - we always hear people say the S&P 500 averages 8-10% returns over the long haul, but WHY is this?

There are a few factors:

Companies tend to grow and generate profits over time, which usually increases the value of their stock.

Inflation causes the prices of goods and services to rise over time, which can increase the revenues and profits of companies.

Lastly, advances in technology and productivity can lead to economic growth and higher corporate profits.

As the economy as a whole grows, the stock market tends to go up as well. This is because as the economy grows, companies are able to sell more products and services, which leads to higher profits and higher stock prices. So long as the economy keeps growing (due to innovation, population growth, and consumption) we should see the market expand over time.

As soon as the Fed starts to cut rates in the next year, that should be a good signal for us to start to deploy more capital into investing.

Enjoy your Sunday!

— Humphrey, Tim, & Rickie

Market Report

In a recent Senate Banking Committee hearing, top US officials discussed the collapse of Silicon Valley Bank (SVB), which catered to the tech and startup industry, and Signature Bank, which had large exposure to crypto. After following the hearing, it’s evident that there’s the potential for the most significant regulatory overhaul of the banking sector in years. Depositors at midsize banks like these have been withdrawing money at a record pace, leading to concerns that banks may become increasingly vulnerable.

The failures of SVB and Signature Bank have led financial regulators to think about buffing up capital, liquidity, and interest-rate risk management for the larger banks. Lawmakers from both sides of the aisle have jumped into the debate too. Republicans point their fingers at high inflation and aggressive interest-rate hikes, while Democrats believe that regulatory loosening during the Trump era played a significant part in the current banking crisis.

Federal Reserve Vice Chair Michael Barr and FDIC Chairman Martin Gruenberg shared some ideas to tackle these issues during their testimonies:

Enhancing the Fed's stress tests of banks with multiple scenarios to uncover various channels of contagion.

Expanding the Fed’s stress test could help identify potential vulnerabilities in banks' capital and risk management strategies, making sure that they have the necessary safeguards in place to withstand shocks to the financial system.

Proposing a long-term debt requirement for big banks that aren't designated as globally significant creates a cushion of loss-absorbing resources.

Having these requirements for banks not designated as “globally significant” could help minimize taxpayer-funded bailouts and promote greater financial stability by ensuring banks have sufficient resources to absorb losses during times of stress.

Exploring liquidity rules to improve banks' resiliency.

Strengthening liquidity rules would require banks to maintain a certain level of high-quality liquid assets that can be quickly converted to cash in a crisis.

The FDIC will present options for potential changes to deposit insurance coverage, currently capped at $250,000.

Changes to deposit insurance coverage could provide additional protection for bank customers, enhancing confidence in the banking system.

Gruenberg called for "serious attention" to the capital requirements for the securities portfolios of banks with assets over $100 billion.

Banks with assets over $100 billion could face increased scrutiny regarding maintaining adequate capital buffers to cover potential losses from their investments.

Extensive investigation into the collapse of SVB and Signature Bank.

Both the FDIC and the Fed are preparing reports on the collapse of SVB and Signature Bank, with plans to release them by May 1.

Despite these proposals, senators from both parties criticized the Federal Reserve for not preventing the collapse of SVB, even after spotting risks beforehand. Michael Barr defended the Fed's actions, saying they did raise concerns with SVB privately before its collapse and gave the lender a thumbs down for risk management. He added that the bank's management dropped the ball on dealing with interest rate and liquidity risks. Senators, however, questioned why the Fed didn't jump into action sooner when they knew about the bank's issues.

Some lawmakers also wondered why the FDIC didn't find a new home for SVB before it went under. They thought this might have allowed the government to dodge stepping in to protect all depositors at both SVB and Signature Bank. FDIC Chairman Martin Gruenberg explained that they did receive two bids to buy SVB, but one was a no-go because the buyer's board hadn't given the green light. The other bid got the ax from regulators because it would cost the FDIC more than simply liquidating the bank. In the end, the government intervened to protect depositors at both banks to prevent further instability in the financial system.

As regulators and politicians grapple with how best to deal with the banking sector, the question remains - how far will the changes go? Will we see a full-on regulatory makeover or just some slight tweaking that leaves the fundamental rules of the game in place?

Forecast Ahead

Markets will be closed on April 7th because of Good Friday.

Big Number

Historically, April has been one of the best months for stocks, with the Dow Jones and S&P 500 closing positively in 15 of the past 16 years. According to Money.com, the Dow Jones has had an average monthly gain of 1.46% in April since 1950, making it the best-performing month in the stock market.

Overcome the Sunday Scaries

Memes of the Week

In Case You Missed It

Partnerships

If you are a brand looking to reach thousands of business leaders and investors through our two weekly newsletters, we would love to hear from you!