💳✉️ Credit Series: How to Make Credit Cards Work for You!

💳✉️ Credit Series: How to Make Credit Cards Work for You!

In the final article of this multi-article credit series, we’re going to talk about how you can take advantage of using traditional credit cards to make them work in your favor without going into debt. This article is for the financially savvy reader who has an understanding of how credit cards work and wants to maximize their benefits.

How Traditional Credit Cards Work

Our last credit series article discussed starter credit cards to help establish and build credit. But those work pretty differently from a regular consumer credit card. Here’s a quick overview of how a traditional credit card works:

You apply for the card. For a typical credit card, lenders will have all sorts of promotions to entice you to sign up. More on that below.

The issuer reviews all of your information, including your employment status and income, debts, etc., to determine your creditworthiness and calculate your credit limit (that is, the most you’re allowed to borrow from them). You’ll likely get a soft credit inquiry on your report.

You’ll get approved or denied for the card in question. If approved, you’ll get your credit card in the mail, where you’ll be informed of the terms, like the credit limit and interest rate.

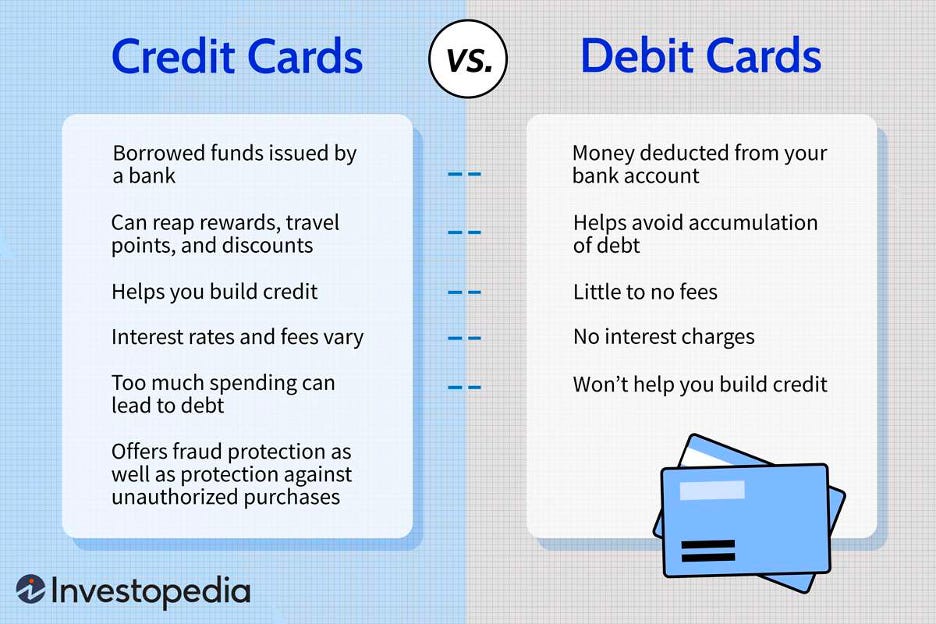

When you use the card, you’re essentially borrowing money from the lender with the promise that you’ll pay it back. Typical credit cards are unsecured loans, meaning that you can spend up to your credit limit, pay it back, and then spend again. Think of it like a revolving door.

You’ll have a minimum monthly payment that the lender calculates for you. This is the smallest amount you must pay each month to keep your account in good standing. If you pay the minimum but don’t pay the card back in full (meaning whatever you spent) each month, your account will be in good standing, but you’ll start to accrue interest. Interest on credit cards is usually a very high percentage and can be an absolute killer, so it’s important to keep your credit card utilization low and only spend what you can pay back each month.

Keep This in Mind!

Before we dive into the many benefits of credit card usage, it’s important that we remember the general risks of credit cards. They aren’t for everyone; in fact, many Americans are not responsible credit card users. That’s because they may not fully understand how they work, and then they make purchases until they’re maxed out and don’t have the money to pay the card back in full each month. This quickly leads to racking up credit card debt, owing even more as interest accrues, and credit scores falling if payments aren’t made on time. If this sounds like you, keep practicing good financial habits and work your way up to using credit cards only when you feel that you can use them wisely!

Benefits of Credit Cards

What if I told you that savvy credit card users make all of their purchases on credit without going into debt or gaining interest while earning rewards simultaneously? On top of boosting your credit score, which we’ve talked about pretty extensively throughout this series, there are some other great advantages that can come with using traditional credit cards.

Protection against fraud

Redeemable perks, like cash back, miles, or points

Easy to track spending

Let’s talk about each of these benefits in more detail.

1. Protection against fraud

Using credit cards for your purchases can actually be safer than using a debit card. This is because your credit card isn’t tied to a checking or savings account like your debit card is. Simply put, the money you spend on a credit card is the card issuer’s, not yours. If you see a fraudulent purchase on your credit card statement, you can rest assured that it’s not your money that was used to make the purchase. If your debit card gets stolen, your own money in your bank account is at risk.

Along with that, if you ever find a fraudulent charge on your credit card statement or something doesn’t look right, it is much easier to dispute a charge and get that credit back; whereas if you’re using a debit card that is linked directly to your bank account, it’s harder to prove that you weren’t the one who made a purchase.

2. Redeemable perks

Keep reading with a 7-day free trial

Subscribe to Hump 🐪 Days to keep reading this post and get 7 days of free access to the full post archives.