💳✉️ Credit Series: Establishing, Building, and Repairing Your Credit Score

The first article of this multi-article series set the foundation for understanding your credit score so that you know what it is and what goes into its calculation. You may be in a place where you’re just getting started with establishing credit, maybe you’re dealing with not-so-great credit, or you’re looking for some tips to boost your score. If any of these sound like the position you’re in, read on! In this article, we’ll offer tips on how to establish, build, and repair your credit score.

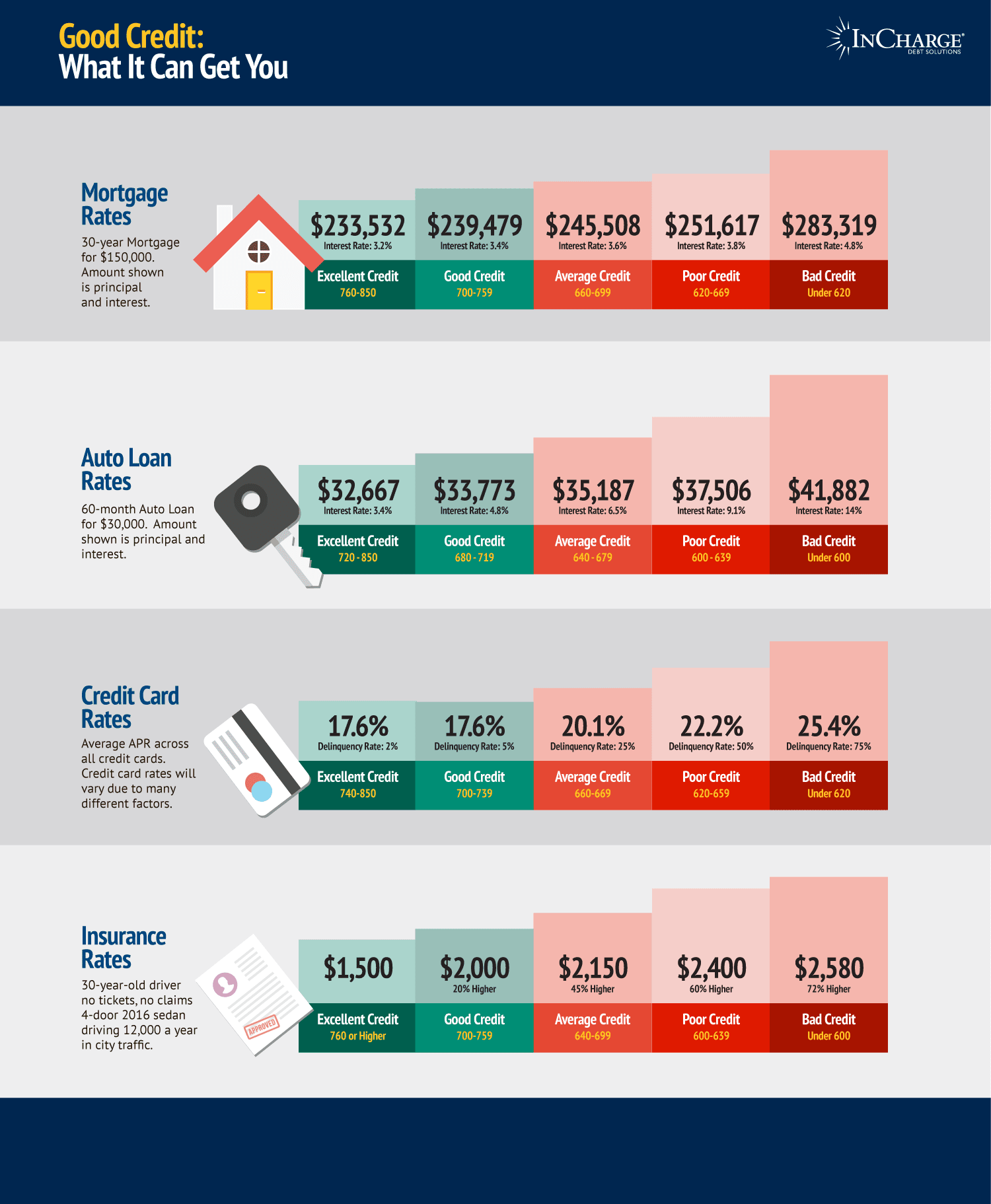

Before we dive into how to build credit, take a look at this infographic, which is a prime illustration of what a good credit score can mean for your bottom line (AKA what you have to pay). This is just an example, but it shows why having a high credit score is so important to your financial health. It can mean the difference of thousands of dollars for your mortgage, car payment, credit card rates, and more.

A Note on Poor Credit

First, let’s talk about having a poor credit score. A credit score in the ‘poor’ category is typically considered under 580. Usually, a score of 700 is the target to start getting better interest rates and odds of approval for loans, but the higher the score, the better your financial health.

Maybe you’ve missed some payments, have some bills in collections, or had to file for bankruptcy. Regardless of the reason for poor credit, it’s great that you’re here and want to get it on track.

It can be challenging to repair a credit score because derogatory marks are serious and stay on your credit report for 7-10 years, depending on what it is. Derogatory marks include:

Missed payments

Account charge-offs

Collections

Repossession (of collateral, like a car)

Default on student loans

Bankruptcy

Foreclosure

Unfortunately, the name of the game with derogatory marks is time. In some cases, you may be able to dispute it, but usually, you’ll have to wait until they fall off your report. The good news is that you don’t have to give up. Even with derogatory marks, you can still focus on building your credit score up. Let’s take a look at some options to get started!

Establishing, Building, and Repairing Credit

All of the following are great places to start if you have little to no credit history or if you want to repair your credit score. There are a few ways to do this, and we’ll go through them all.

Open Up a Credit Card

Credit cards are a great way to start off on your credit journey, so long as you understand the terms and don’t go overboard on spending.

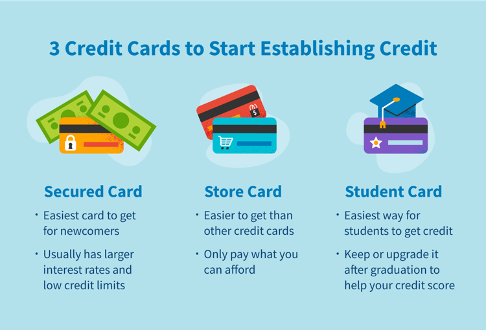

There are three different types of ‘starter’ cards for people who are trying to establish and build credit:

Secured cards

Store cards

Student cards

These are a bit different from typical credit cards. Sit tight, because we’re going to talk all about traditional credit cards in the final credit series article! For now, let’s talk about the starter cards in more detail.

Keep reading with a 7-day free trial

Subscribe to Hump 🐪 Days to keep reading this post and get 7 days of free access to the full post archives.