🐫 A Special Letter: More Hump Days

Thank you for being a loyal reader and welcome to a special edition of the Sunday Primer!

I started this newsletter in June of 2020 and it’s exciting to see how far it has come. The mission of Hump Days is to keep you informed about what’s going on in business, finance, and tech without making things more complicated than they should be. In spirit of that mission, we have an announcement: we’re launching a paid subscription.

The two free newsletters on Wednesday and Sunday you’ve grown to love will remain unchanged but by subscribing, you’ll get access to a bonus, premium article once per week, starting this Thursday. Subscribing is completely optional, and you can follow along the free editions for as long as you’d like!

Paid subscribers can expect detailed dives into companies (our first article is on Microsoft), as well as comprehensive guides that equip you with knowledge on topics ranging from credit, real estate, money management, investing, and retirement.

My favorite analogy is that wealth is accumulated by stacking chips: as you learn more and implement what you learn - these actions compound over time, your wealth stacks up like chips, bit by bit. Our premium articles are offered to arm you with knowledge and stack those chips higher.

Click the button to support us, and read on to learn more about what’s included.

🐫 New features for our paid members (starting soon!)

Access to The Bottom Line: Detailed Company Analysis + Industry Coverage from Our Hump Days Markets Team

Access to The Briefcase: Comprehensive, Easy to Follow Personal Finance Guides Arming You With Financial Literacy.

⚡ Pricing

Monthly at $19.99/month

Annually at $199.99/year (A 16.67% discount)

As an offer and a huge thank you to all our readers, we’re offering 30% off for your first year of membership if you sign up in the next 10 days.

(If cost is a barrier to accessing our content, or if you’re a student, email us, and we’ll work something out.)

Now, onto our Sunday Primer!

— Humphrey

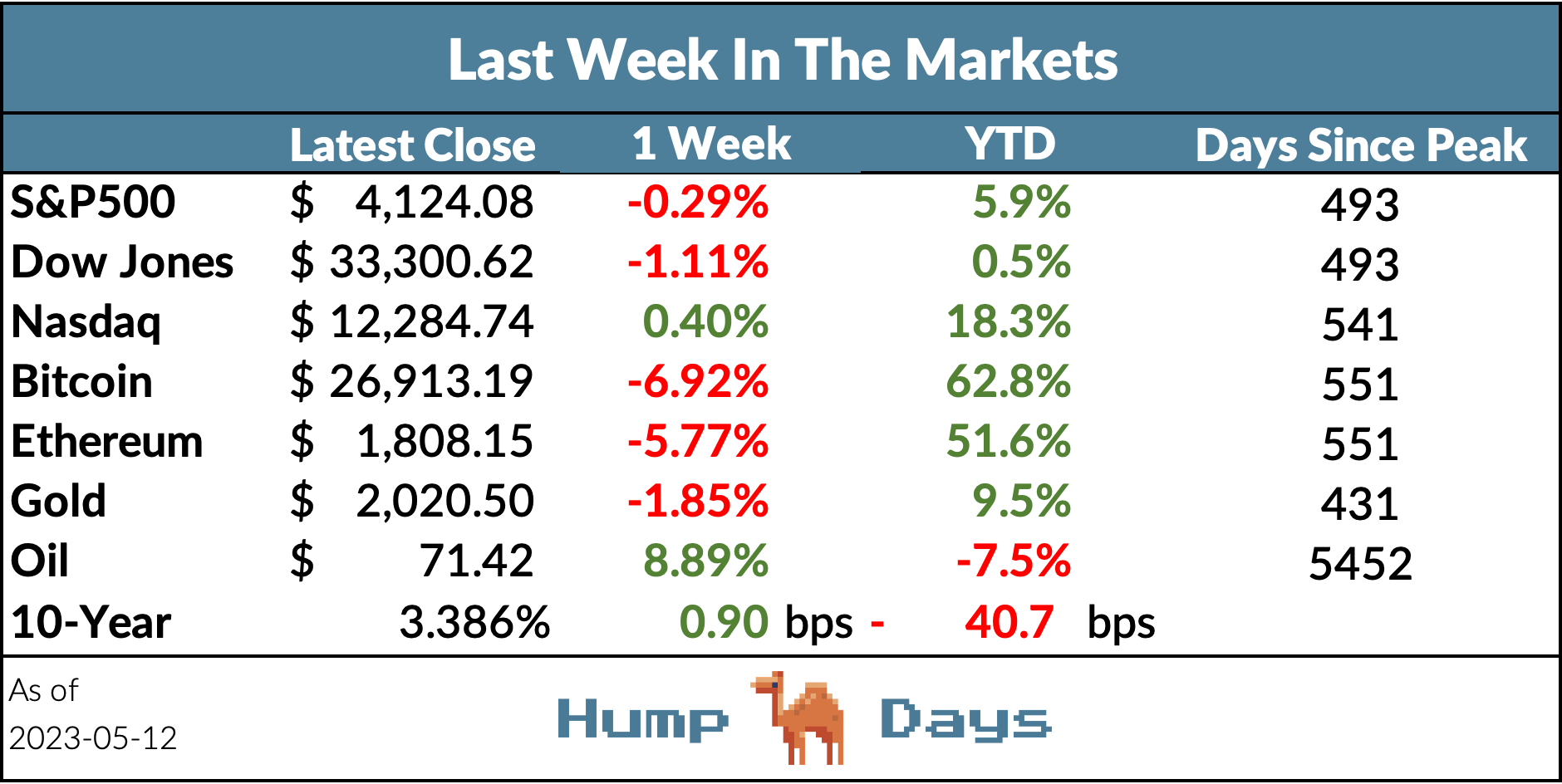

Market Report

Inflation Remains High.

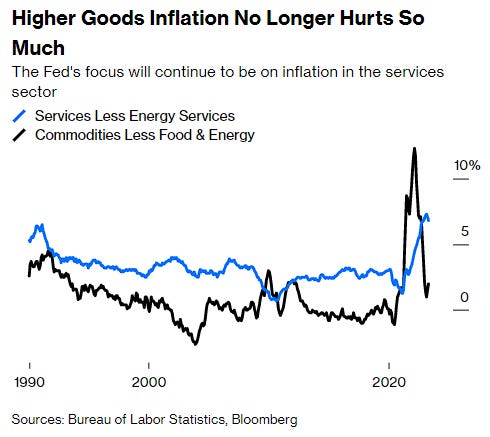

U.S. inflation numbers for April came in below expectations, reinforcing market sentiment that the Federal Reserve may halt its rate hikes in June. According to a Bureau of Labor Statistics report, the consumer price index (CPI) rose 4.9% year-on-year, the first sub-5% figure in two years. Both overall and core CPI (excluding food and energy) rose by 0.4% for the month, indicating a slowdown from last year's high levels, although still above the Fed's target of 2% inflation.

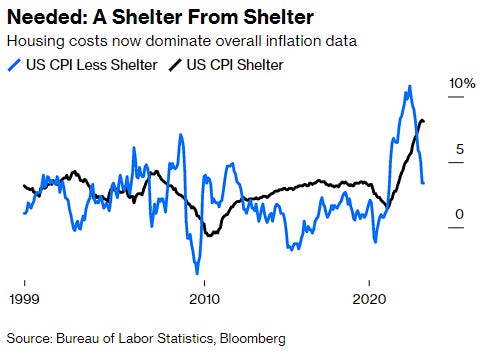

The cost of shelter, which is the largest component of services and comprises about a third of the overall CPI index, rose by 0.4% last month, the smallest increase in over a year. Given that shelter accounts for a significant portion of the overall CPI, any potential decrease in housing inflation from the current monthly rate of 0.4% would significantly influence the overall inflation scenario. Prices for airfares, hotel stays, and new cars saw a decline.

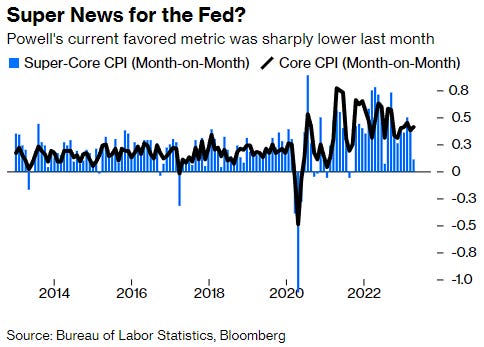

Fed Chair Jerome Powell has been paying special attention to the "supercore" CPI, which excludes housing costs. This measure rose by a mere 0.1%. The central bank's focus on this metric is due to its sensitivity to the tight labor market. Used car inflation, a notable trend from the pandemic, contributed to a slight increase in goods prices.

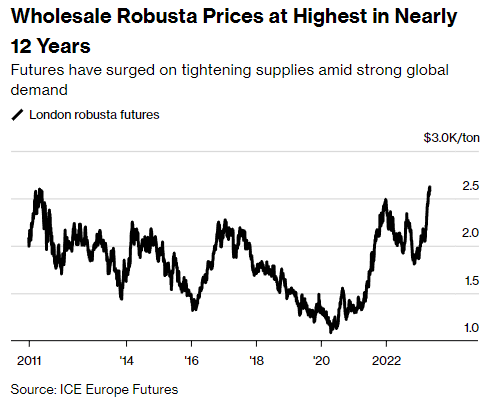

Coffee Bean Shortage?

The global inflation crisis has led coffee drinkers to seek cheaper alternatives, leading to a significant surge in demand for robusta beans, typically used in instant coffee, espressos, and ground blends. However, bean growers are struggling to keep up with this increase, causing prices to reach their highest in almost twelve years.

The world's largest robusta producer, Vietnam, had its smallest harvest in four years as farmers shifted to more profitable crops due to soaring fertilizer costs following Russia's invasion of Ukraine. Additionally, Brazil's crops have been affected by drought, and there are fears over Indonesia's output following heavy rainfall. Despite these challenges, global robusta exports in the first six months of the current season have increased compared to the last three years, but not fast enough to meet the heightened demand.

Gig Economy in Recession?

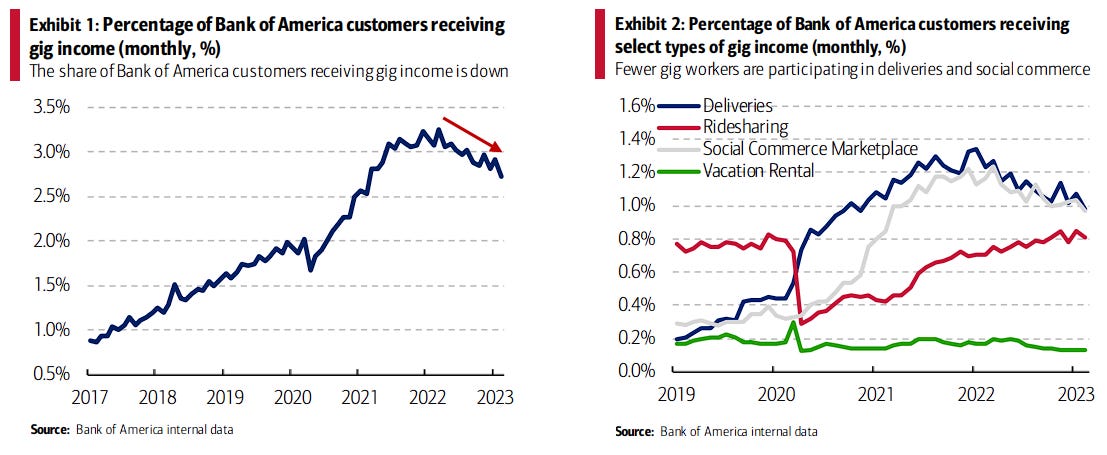

The percentage of Bank of America customers receiving income from gig-type work has fallen to 2.7% in February 2023, down from 3.3% in March 2022. This decline is attributed to both a decrease in demand for services like restaurant takeout and grocery delivery as the economy reopens and to a shift from gig work to traditional employment due to strong wage growth in sectors like retail and restaurants. This rotation could also partly explain the recent increase in the labor force participation rate among younger workers.

On the demand side, there's been a significant decrease in people working for delivery and social commerce marketplaces, despite a slight uptick in ridesharing. The declining demand for restaurant and grocery deliveries as economies reopen has impacted gig workers in these areas. Additionally, those who continue to work delivery gigs are doing so less frequently, and there's been a general decrease in demand for goods.

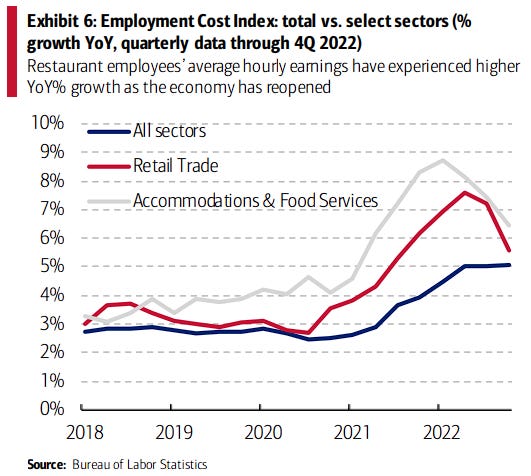

On the supply side, increased wage growth in traditional job markets has likely led some gig workers back to these sectors. Gig workers who also have traditional employment are most commonly found in the retail and restaurant industries. According to the Bureau of Labor Statistics Employment Cost Index, these sectors have seen the largest wage and salary increase in the past two years. Meanwhile, there has been no significant increase in the average monthly income from gig platforms. This could lead gig workers to either reduce their gig work or leave the gig economy altogether. Particularly among Gen Z workers, this dynamic could be driving an increase in labor force participation as they transition from gig work to traditional jobs.

Do you have a side gig or side income that complements your main job? Let us know in the comments what type of side gigs you guys have going on!

Forecast Ahead

Big Number: 4th straight week

Bank shares fell for a fourth straight week, and maybe it’s no surprise that eight of the 10 worst performers in the S&P 500 this year are financials. The collapse of Silicon Valley Bank and other lenders over the past two months has fueled widespread concern that others would be hit by a similar combination of rising costs and mounting losses as higher interest rates weigh on the economy.

Overcome the Sunday Scaries

Memes of the Week

Partnerships

If you are a brand looking to reach thousands of business leaders and investors through our two weekly newsletters, we would love to hear from you!